What are

/r/PersonalFinanceCanada's

favorite Products & Services?

From 3.5 billion Reddit comments

The most popular Products mentioned in /r/PersonalFinanceCanada:

The most popular Services mentioned in /r/PersonalFinanceCanada:

You Need A Budget

Wise

Wave

Mint.com

freeCodeCamp

XE.com

MarketWatch

Have I been pwned?

Schwab

Privacy.com

Bitwarden

Hotels.com

Stripe

Upwork

GnuCash

The most popular Android Apps mentioned in /r/PersonalFinanceCanada:

Spending Tracker

Call Recorder - ACR

TD MySpend

My Stocks Portfolio & Widget with Cryptocurrency

VoIP.ms SMS

Expense Manager

Mortgage Calculator

TD Canada

Scanbot - PDF Document Scanner

Android Pay

Unit Price Comparison

Firefox Browser fast & private

Flipp - Weekly Shopping

FuelLog - Car Management

The most popular VPNs mentioned in /r/PersonalFinanceCanada:

The most popular reviews in /r/PersonalFinanceCanada:

Without question, a bidet.

- Low cost ($30ish on sale).

- You feel cleaner.

- You save money by using less toilet paper so it pays itself off eventually.

- Eco-friendly.

- Easy install.

https://www.amazon.ca/Luxe-Bidet-Neo-110-Non-Electric/dp/B009ZLRSJ6

As someone mentioned in a post over at /r/personalfinance this weekend, there's a huge selection bias when you ask posters to state their income. Those making more money are just more likely to post.

Always treat these 'security questions' as additional passwords. I do that, then store them in my password manager (KeePass2). That way a) no one that knows you would be able to know the answer and b) you don't need to remember them.

Love this post.

If I may be a rampant communist for a moment, I think the reason TFSA will be vilified is because savings is evil and consumption is a virtue in our present culture of consumerism. Save for retirement? Down with the 1%! (Most 1%ers/millionaires are retired and had average incomes according to The Millionaire Next Door) Get a ludicrous home loan that takes three decades to pay off, fancy cars, the fastest economic growth in history, go on vacations, and retire poor? Gotta get those millennials to pay more into CPP.

Not saying consumerism is bad though ;) Just that it makes those who save look bad and those that consume look like those who need help.

The TL,DR of "economic outpatient theory" in The Millionaire Next Door is: people who give their kids money have kids who are under- accumulators of wealth relative to people the same age, but whose parents didn't give them anything.

The "lesson" from the book is "don't perform economic outpatient care" on your kids - instead, raise them to be financially self-sufficient.

A good read for the downside risk and lots of food for thought: Hilliard MacBeth - When the Bubble Bursts

https://www.amazon.ca/Millionaire-Teacher-Wealth-Should-Learned/dp/1119356296

also

Stop Over-Thinking Your Money by Preet Banerjee

There are a bunch of good Canadian finance reads but I would start with those 2.

If you want more economic reasons to feel good about biking to work, I just finished reading this book & would definitely recommend: https://www.amazon.com/Bikenomics-Bicycling-Save-Economy-Bicycle/dp/1621060039

It might look a bit hippie but it's really accessible, interesting and well-researched. As someone who has never owned a car, the figures about how much car ownership costs are staggering.

If someone wants to do the same for Android, this app comes in handy for doing sms https://play.google.com/store/apps/details?id=net.kourlas.voipms_sms

I can't speak to if this one works or not on iOS, but here https://itunes.apple.com/ca/app/voip-ms-sms/id1037874743?mt=8

No lease.

It is the most expensive and worse way to own a car. Buy a used car within your budget outright.

You actually have a great start compared to many and with a bit of knowledge, you will be very well set up for the future. I really suggest you reading some of the recommended books as no comments will be able to extensively cover all aspects.

Read these:

- The Richest Man in Babylon

- The Millionaire next door

- The Millionaire Teacher

- The Wealthy Barber

You will find that most of personal finance is to avoid lifestyle pitfalls and being able to save money to be 80% of it. Then investing to be actually the last 20%.

Best of luck.

Edit: One of the pitfalls is leasing a car.

Sorry for your loss..

Given your financial position (able to support yourself through school without borrowing) I would invest in ETFs, something like a Vanguard ETF with a minimal MER. I'd also transfer that mutual fund over to the same ETF as the management fees are typically too much, eating away at your returns. Even though the management fees may seem small, compounded over X years to retirement at age 21 is seriously significant..

If you invest this inheritance at your age and follow something like the 4% rule, you'll be retired before most people even start saving for retirement..

If you don't really follow what I'm saying, I highly suggest reading Millionaire Teacher.

https://www.amazon.ca/Millionaire-Teacher-Wealth-Should-Learned/dp/0470830069

'Equities' means stocks. If you're saving for the long term, you probably want to have mostly equities right now. I'm assuming you're fairly young.

Incidentally, 55 is not old, and it will be on you before you know it. I've known a few folks who thought they would be retired at 55. They're not.

You seem like a literate guy. Don't jump into anything your bank offers you right away. They tend to sell expensive products (mutual funds, 'portfolios') which may not perform very well. Do some reading-- everyone here advises you read books like The Wealthy Barber and The Millionaire Next Door, and I can't argue with that. (I've never read either myself.)

If you Google the Canadian Couch Potato blog by Dan Bortolotti, you'll get all the information you need on passive index investing, which most people would say gives you the most return for time invested. You can get high-quality investments for a ridiculously low management fee in 2017, but the investment dealers (think Investors, Edward Jones) and the banks would be happy if you didn't know about them. (An exception is the TD e-series funds, which are inexpensive index products).

With 20 to 40 hours of reading, you can be doing it yourself, and then you only need to revisit your portfolio once to a few times a year. Good luck, and happy investing!

Perhaps write a letter to Attn: Legal, asking them if you'll need to go to small claims court to get the funds releaed.

Paypal Canada is under Ontario law, so actually pursuing them in small claims court probably won't be cost effective for you unless you live there.

EDIT: More information follows.

The Paypal Canada agreement has a paragraph on how to pursue binding arbitration, without actually having to go anywhere. https://www.paypal.com/ca/webapps/mpp/ua/useragreement-full

I've just started using YNAB for the past two months and it has helped me a ton so far. It imports all my transactions from my Bank (RBC); you can check to see if it is compatible with yours. https://www.youneedabudget.com/

The Couch Potato Strategy work because:

- Over the long run, the market rises. Yes, bear markets happen. Every eighteen months. But the bull is real and cleans up.

- Fees in managed accounts (ex. Mutual funds) eat away at gains. Example, a 1% fee in year one is equal to a 4% fee 30 years later on that initial inventment assuming comically modest returns (0.01 * 1.05^30 = 4%). It is 32% if you assume the thirty-year average of 8.5% (?I think?).

- People's natural impulse is to buy high and sell low. This is bad. Couch potatoes don't make this mistake.

- Over the long run, the market rises.

- Many stocks fail. They get eliminated. The ones that survive, thrive and new ones come along with drastic growth. Unless you're psychic or talented, you are probably going to pick the stocks that will fail and miss the growth and thriving ones.

- Even if you are a professional, you likely don't have the discipline to handle picking your own stocks. In The Millionaire Next Door the authors explain their data on how investment brokers' tend to have their own portfolio underperform their clients'. Even though they save on their own fees! The reason? They get scared when they see one of their investments tank by 50% and sell it.

- Over the long run, the market rises. Even if you invest at the peak of the market you with index funds, over the long runs you'll have good returns. Look at the case of unlucky Bob, the world's worst stock timer who only buys at highs: http://awealthofcommonsense.com/2014/02/worlds-worst-market-timer/

This math is useful, yes. I've used similar math to evaluate commuting method (bike, car, bus, walk). Accounting for the added cost of a car and my net (after tax) hourly rate, I can figure out "adjusted speeds".

For example, if driving takes 15 minutes and cycling takes 45 minutes, but I spend 30 minutes of my day working to pay for the average daily cost of my car while only 5 minutes of my day to pay for the average daily cost of my bicycle, then a bicycle is only roughly 5 minutes slower than driving, not 30 minutes slower.

In my case the numbers above are pretty damn accurate. Here's the spreadsheet I made if people want to prove me wrong/use it themselves.

It's not staff members. Online accounts with the same email/password combos get leaked and 'hackers' will use this information to try and login to your optimum account. The email and password is all a hacker needs to redeem points.

You can check if any if your email and password combos have been compromised at haveibeenpwned.com

I'm going to use this post to shameless plug my free to play, minimal ads mobile Android game, Deep Ship Alpha!

https://play.google.com/store/apps/details?id=com.FCCompany.FCsAwsomeGame&hl=en_CA&gl=US

I'm so far $4.95 richer and have a sequel in the works.

It's worth noting that until I've generated 100$ worth of game rev, I can't transfer the money XD

I bought a hair dryer round brush. So instead of blow drying your hair then straightening it, you blow dry it with the brush and it gives you a lovely, shiny blowout. This is the one I have.

My entire hair game has changed - my hair is much longer, looks incredibly healthy (and is), looks thicker and fuller, has less breakage, etc. My hairdresser was like what’s your secret your hair looks so great. Best $50 I’ve spent on amazon for sure.

What do people think about this article, that I am sure has been discussed before?

**the numbers presented in the article/post are in USD.

I am aware that there are some pretty big assumptions in his math, but there are also some good points that are worth talking about.

I think the most important thing is: how do you value your time when you are not at work. Without putting a number on that, it is difficult to do any calculations of mortgage vs commuting.

I come from a similar educational background. I ended up in environmental consulting after a decade in oil and gas, early in my career.

Why don't you look at asbestos related jobs? Asbestos abatement was my saviour in transitioning away from oil and gas at the best possible pay. Abatement companies and consulting firms are always hiring, nationwide. Your education credential will get your foot in the door.

I wrote a book about asbestos identification and removal along with my exposure(s). If you are looking to learn more about the industry please check it out.

https://www.amazon.ca/Asbestos-Exposed-definitive-identification-including-ebook/dp/B08H2KS528

Free for Amazon Prime members.

Came here to recommend Wealthing Like Rabbits. I've read all the books recommended in this post (so far), and this is the only one I would recommend in this situation.

It's Canadian, it uses very tangible examples, it discusses RRSPs and TFSAs and sprinkles in zombies and 'multiplying rabbits' metaphors to help clarify concepts like interest rates.

One of my favourite personal finance books entirely because I learned a few things and it gave me a chuckle.

Edit: Here's a link

Congratulations! To anyone else looking for guidance in this area, I strongly recommend reading Getting to Yes. https://www.amazon.ca/Getting-Yes-Negotiating-Agreement-Without/dp/0143118757/ref=sr_1_1?keywords=getting+to+yes&qid=1576216449&sr=8-1

Recently bought a new 64gb xiaomi note 7 for $250 and had it delivered in two days. Best phone I've ever had.

Edit* for the people pming me for a link here it is it's on the murican version https://www.amazon.com/Xiaomi-Redmi-Note-Snapdragon-Black/dp/B07PY52GVP

The most impactful books I read were (in this order).

- The Millionaire Next Door

- The Wealthy Barber Returns

- The Millionaire Teacher

2 and 3 are both written by Canadian Authors so they talk about TFSAs, RRSPs, Pension and Tax that will suit your situation.

Well first of all, you shouldn't be investing in anything while holding a 9.1% line of credit! If you can afford $1500 out of your chequing right now, you should pay that off - otherwise direct your $40/week savings towards getting rid of that. Your Tangerine balanced growth investment is not going to be earning you 9.1%, so by continuing to invest in it while holding that debt is just throwing away money.

Next I'd pay off your car loan as fast as you can... for the same reasons. In terms of the amount you'll save on interest, it's equivalent to getting a tax-free investment that returns 6.1%.

Holding individual stocks in companies such as Apple is a bad idea... you stand to lose a lot of money if something bad happened. I suggest you read up on the advantages of index investing (which is what the Tangerine mutual funds are doing). Books like Millionaire Teacher, or The Little Book of Common Sense Investing are good sources. As is the Canadian Couch Potato website.

So my advice would be to sell the stocks in that RBC TFSA account, use however much you need from it to pay off both debts, then put the rest in Tangerine's TFSA. If you only need $5000 or so in the short-term, then maybe just put that much in the Balanced Growth fund and put the rest into a more aggressive fund (depending on how long you anticipate holding it for, and your personal risk tolerance).

Here is the last snapshot before he changed the model portfolio page.

| Asset Class | Allocation | ETF |

|---|---|---|

| Canadian equity | 12% | PowerShares FTSE RAFI Canadian Fundamental (PXC) |

| Canadian small cap | 6% | iShares S&P/TSX SmallCap (XCS) |

| US equity | 12% | Vanguard Total Stock Market (VTI) |

| US small-cap value | 6% | Vanguard Small-Cap Value (VBR) |

| International equity | 6% | iShares MSCI EAFE Value (EFV) |

| International small cap | 6% | iShares MSCI EAFE Small Cap (SCZ) |

| Emerging markets equity | 6% | Vanguard FTSE Emerging Markets (VWO) |

| Global real estate | 6% | SPDR Dow Jones Global Real Estate (RWO) |

| Government bonds | 20% | BMO Mid Federal Bond (ZFM) |

| Corporate bonds | 20% | Vanguard Cdn Short-Term Corp Bond (VSC) |

I considered the field a couple of years ago, but gave up on it mostly since I don't like the "taking people to court" thing, not for me. While most lawyers are nice people, I find that my life is a lot better if I limit the amount of contact I have with them.

Look up the ACFE (.com). Private firms would probably be the smartest move for a career in that field but you will also need your CPA. Their work is more of a service to their clients and does not always involve going to court, but can lead to it.

For CRA poster, you will probably be working in investigations, so expect to have to be very detail oriented since any actions they do is to bring someone to court (very different mind set compared to auditing). So they have to show everyone who touched or had access to any piece of evidence otherwise it will thrown out of court. I'd look up "Mens rea" in Canada if you are serious in applying to CRA.

If you are really interested in this field, I'd recommend this book:

Fraud Casebook Lessons from the Bad Side of Business by Joseph T. Wells

https://www.amazon.ca/Fraud-Casebook-Lessons-Side-Business/dp/0470134682

It's got good stories on fraud cases, I'd pay attention to the timelines. Most cases can take a LONG time to bring to court, let alone have it resolved in court. Still an interesting read, but the cases start to be a bit repetitive halfway thru.

I would recommend doing some reading before doing anything with this money:

Millionaire Teacher

A Random Walk Down Wall Street

The Wealthy Barber

This is ALOT of money, so also make sure that you don't go around telling friends/family and even financial advisors about this inheritance, because they will come running. Do your due diligence, you have the opportunity to snowball this money to feed and clothe future generations (if youre going to have kids/already do) :)

/u/whusts's arguments are good, I'll give a couple more points.

I didn't real the full post since it devolved into ranting, but the main thesis was professional managers can do better than DIY/indexing because they have more experience.

Think of it this way. If you buy the index, you will (modulo fees/noise) match the return of the aggregate of all investors - that's exactly what the index is. Some will outperform you, some will underperform, but you will match the mean. Secondly - most money is professionally managed. Putting this together, it's impossible for the mean professional to beat you if you are indexing. The only way you can if you're from Lake Wobegon, where all the investing professionals are above average. The reason indexing does better than the mean professionally managed funds is the fees are lower.

There's been a lot of research into this. You can start with A Random Walk Down Wall Street.

Norbert's Gambit is indeed the cheapest. Assuming your pay isn't in a physical cheque, you can check out places like KnightsBridgeFX or Wise to see if they can convert the funds for you.

If your employer is US based, it might be better if you get a Wise Multicurrency Account, get a US account encoding number and have your employer pay you there and then have Wise do the currency conversion and send that money to your Canadian bank account.

For more on this: https://wise.com/ca/multi-currency-account/

{kind=link}

{kind=link}

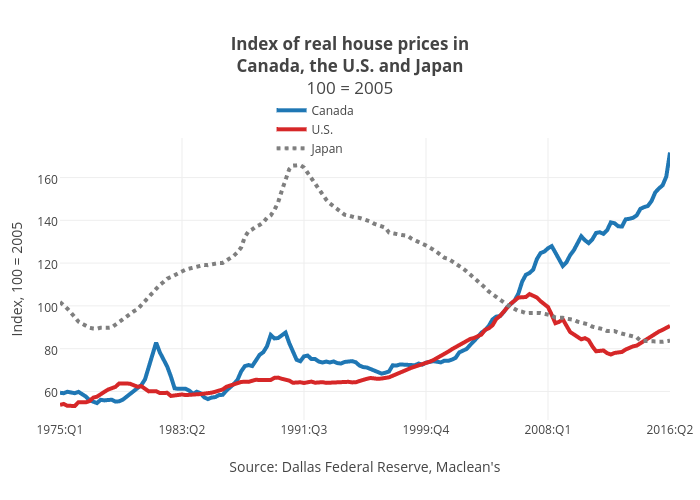

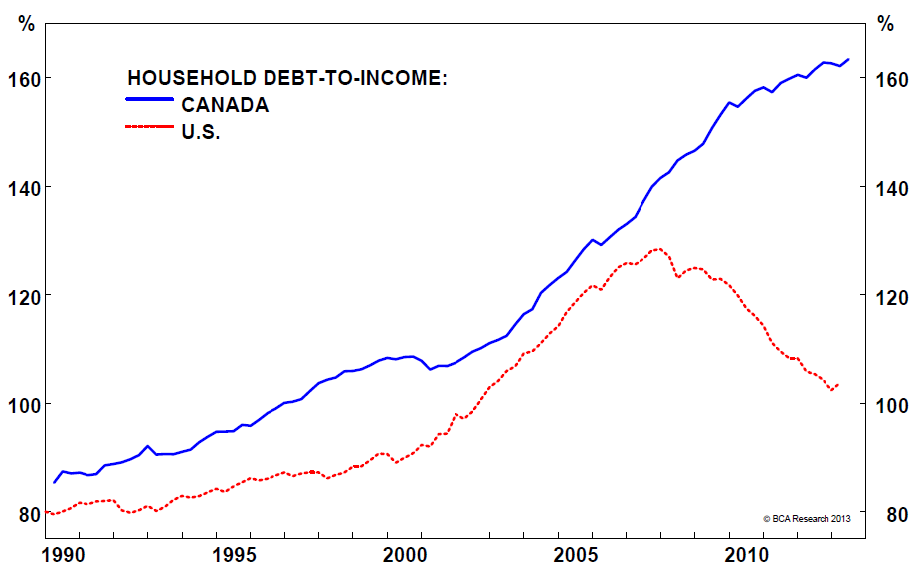

It seems to me that if foreign investors were really "pricing us out" then the personal debt curve wouldn't be as dramatic. It looks like canadians are being priced out by canadians more than anything else.

I use YNAB's software to budget and find it a lot slicker than the several spreadsheets I made trying to copy it before deciding to subscribe. There's a regular thread where people share their categories over at r/ynab.

It took some time to fiddle with the categories I use and decide how to bundle / separate everything. And as circumstances change I'm sure my categories will change again. A budget isn't something you come up with in an afternoon, it's something that takes months to get the hang of and will always be evolving. It's all about your priorities.

Currently I have my categories organized under six groupings:

- Immediate Obligations (aka "need now": groceries, monthly bills)

- Irregular Bills ("need later": quarterly and annual bills)

- Irregular Expenses ("need whenever" & can choose to cut back on if necessary: clothing, household goods, etc.)

- Treat Yo Self ("want now": entertainment, dining out, etc.)

- Goals ("want later": saving for big ticket items, upcoming vacations, etc.)

- The Banana Stand (there's always money in it: emergency fund, home reno fund)

Money for my "now" & "whenever" categories is kept in my chequing account, money for my "later" categories is kept in my high-interest savings account, and my "banana stand" is my high-interest TFSA.

​

PS - Do not invest your emergency fund or money being saved for a car you plan to buy within the next decade. Do not invest anything until you reach Step 5 of the Money Steps. You're currently on Step 0.

>Will eventually come to Canada.

The reason American brokerage fees went to zero was that the fees were already a small part of brokerage revenues. The majority of the money was coming from payment for order flow, interest on margin loans, etc. Payment for order flow is specially notable, and is the main source of income for Robinhood:

>When you buy or sell stocks, ETFs, and options through your brokerage account, your orders are sent to market makers for execution. To compete with exchanges, market makers offer rebates to brokerages. Market makers typically offer better prices than exchanges. [Source]

Payment for order flow is not allowed in Canada. In the absence of this revenue stream, I do not expect Canadian brokerage fees to ever go to zero.

A 9 week web development course is not worth $10k. If you have no or little programming experience, the first 3 weeks at least will be teaching you basic programming concepts that can be learned very easily online for free:

- a crapton of programming classes are on www.coursera.com,

- Udacity is very well known for their programming 'nanodegree' as well: https://www.udacity.com/, or

- a course on HTML5 run by the World Wide Web Consortium is starting in October: https://www.edx.org/course/learn-html5-w3c-w3cx-html5-1x-0.

Plenty of very advanced and narrowly focused courses as well. All free and readily accessible.

And these days, there is no one specific skill called "web development" -- in the last 5-6 years there has been an explosion of programming languages, tools, standards, libraries/toolkits etc to the point that there is a very diverse landscape from simple webpages, to Wordpress-style content management systems, to Software-as-a-service madness using Amazon Web Services and the like.

Software development is probably the most learnable skill online.. dont waste cash on it.

This graph from Maclean's shows that in the US the average real house price in the US in Q2 of 2016 was lower than it was in 2008. Their prices bottomed out in about 2012.

A knife sharpening kit, it turns cheap ikea knife sets to razors, and you can re-sharpen whenever it starts to dull.

Pro-tip: grab one that sets the angle and keeps it there, makes the process a 1000% easier. I use the DMT Deluxe Kit DMT Kit

Great job! You've learned a very valuable lesson that will pay dividends for your whole life: Delayed Gratification.

If you can happily maintain a 50% pay yourself first savings rate without mental health/social/living life issues than continue to do so. Your savings today will magnify over time and financial independence at a young age is possible.

Here's a good book if you haven't yet been introduced to the idea: https://www.amazon.ca/dp/0525538690/ref=cm_sw_r_cp_apa_i_ICggFbCGAP6JN

The Wealthy Barber and The Wealthy Barber Returns for basic household finances. Canadian

The Value of Simple for the basics of Investing. Canadian

The Lazy Investor to understand DRIPs. Canadian

The Intelligent Investor is the bible for EDIT: value investing and is noted by Warren Buffett as one of the best investing books ever written. US based, but very applicable no matter where you are

Very low risk? GICs and HISAs.

But your plan to buy ETFs after the market has crashed is foolish. You don't know when the market is going to crash. All sentiment and risk is already priced in. Unless there's something you know that nobody else does, you will lose by playing this game. Grab a copy of "A Random Walk Down Wall Street" to really have your eyes opened.

Determine your risk tolerance, pick an asset allocation, and stick with it for the long term. This has repeatedly been demonstrated to be the best way to get reliable returns.

If your risk tolerance is very low, GICs and HISAs all the way. If it's a bit higher, maybe try 30% equities/70% bonds.

You owe your dad better than gun-slinging management of his nest egg. His advisor screwed him over, don't you go do the same thing in a different way. If you're planning on acting as his financial advisor, you have some homework to do.

Millionaire Teacher

A Random Walk Down Wall Street

Four Pillars of Investing

The Intelligent Investor

If they're already retired (you mention 'income'), you need some books on managing a portfolio during retirement. I am young and haven't faced this challenge yet. This page: https://www.bogleheads.org/wiki/Books:_recommendations_and_reviews has a dedicated retirement reading list. If they're retiring and you haven't run monte carlos against a variety of different withdrawal rates, you haven't even started your job yet.

Sorry if I came across as a dick. I just hope you take your responsibility seriously.

I read everything I could get my hands on. I liked Robert Hagstrom's books on picking stocks like Warren Buffett. I thought Mary Buffett and David Clarke's books were very good as well. I loved The Intelligent Investor, practically memorising the thing. Lawrence Cunningham's Essays of Warren Buffett is also an excellent read, as are all of Buffett's letters to shareholders. Philip Fisher's book, Common Stocks and Uncommon Profits is worth reading for every stock picker. I also highly recommend Schilit's book, Financial Shenanigans. It shows how to find the sneaky deception in annual reports. I used to also read (back to front, because the juicy stuff is always at the back) 10 years worth of annual reports for any stock I was interested in buying. In addition, I always read the financial reporting at Valueline.com for each company I was interested in. Why did I switch to a portfolio of index funds? It's a heck of a lot easier! I used to own common stocks and index funds. But there are challenges with common stocks. If you are rebalancing a portfolio, do you sell some Coke, WalMart or Berkshire Hathaway at the end of the year? If you are adding fresh proceeds to your portfolio, which stock do you add to? This was easier when I had less than a million dollars in my portfolio. But as my money grew, the stakes grew with it. Few investors beat a portfolio of index funds over an investment lifetime. Some might point to a decade of doing so, thinking that they have the special skill to beat the market. For years, I was one of those guys. I had done well for at least a dozen years. But smarter guys than me eventually paid the piper. Eventually, most people lose to the market index. So...I decided that fully indexing my portfolio gave me more free time to spend with my wife, travel, while providing me higher long term odds of success (30 years +).

I really recommend everyone read "The Richest Man in Babylon". Published in 1923 and most of it still rings true today. Well-written and a pleasure to read.

Also www.Canadiancouchpotato.com . Moneysense rated it the best financial blog in Canada last year. It's an excellent resource.

I looked into this some time ago as well. A lot of people are recommending bitcoin ATM's, but be aware that the service fees for these machines can be really, really high. I get it, it costs money to provide a service, but look up the rates ahead of time so you're at least aware of how much you'll be paying.

(https://coinatmradar.com/blog/bitcoin-atm-fees-2016-revision/) - This site says average in canada is 7.5%, but I recall fees in the range of 10-15%. Buyer beware.

Other suggestions - if you use Android, the Mycelium Bitcoin wallet has a Buy/Sell Bitcoin feature that can connect you with local users for cash transactions. I never used it myself, but it might be a cheaper alternative. (I found Mycelium to be a great wallet by the way - https://play.google.com/store/apps/details?id=com.mycelium.wallet&hl=en)

Yo this hits close to home. I'm making roughly the same, am a few months older than you, and have a bit more owing to OSAP than you.

Breathe though.

First, you absolutely NEED to get a handle on your monthly budget. There is just no way for you to do this quickly if you aren't even sure where your money is going.

I'm not saying you have to make decisions about what stuff to cut down on, etc right now, but you need to be honest with yourself for your own good. A good exercise is to pull statements from the last three months of your accounts (credit cards (all of them), bank accounts, etc) and start to put together a typical month of income and expenses.

Once you figure that all out, you need to honestly ask yourself if paying off OSAP is a priority for you. Up until now, it clearly hasn't been; as you've been paying for train tickets and Airbnb (sounds like you are going on short trips, unsure if they're work related or not).

It's up to you; but you really ought to do this. Check out the You Need a Budget book (the public library has copies). The site (https://www.youneedabudget.com/method/) has a good intro to the method behind the software. You don't need the app necessarily, but you might want to really give the methodology and method a good look.

Once you have your expenses, and have set your priorities; give you dollars jobs and stick to it.

It sounds like you are paid bi-weekly, so you have 26 pay periods in a year. Great. Budget monthly on the assumption of 2 pay cheques per month. Operate as if you were only paid 24 times a year. The extra two payments can then be put right into debt, because it's gravy.

https://www.remembear.com is good for people frightened at the options in more complex password managers.

Tried to get my parents set up with 1pass long ago and they just couldn't figure it out. They seem to get by with Remembear though! (I like 1Pass better but I can understand it's hard to use if you're not technically savvy)

There's camelcamelcamel for Amazon, which shows the price history and price alerts. But I don't think there's much furniture there. Then there's Honey, which applies coupon codes automatically on many sites.

Graham was a genius because he believed in investing and not in speculation.

The way one invested before index funds were available, and when markets were less efficient at pricing in information, was quite different. In a time when the only way to play was to choose stocks, you needed a level head like Graham to keep you away from buying hyped up junk with your retirement money.

He didn't believe in diversifying beyond the number of stocks you could manage to understand the fundamentals for; so, if I recall correctly, he'd have you hold maybe 30 stocks. This addressed a human limitation, not a financial one. According to John Bogle, he actually told Warren Buffet that he was an indexer in his later years.

Surely you must see how logic alone shows you how the fundamental analysis approach you're taking (security analysis, valuation, etc.) is of little benefit when all of the information is already priced in. A highly efficient market leaves little room for finding value (I assume you consider yourself a value investor) or any other kind of alpha. By your logic, everyone could achieve better than average returns if they'd only hire someone with a 'team of analysts'? You fail to understand what an average is. Remember, half of the working analysts currently trading (and thus setting security prices) are underperforming. How can you be sure your team will best the average? And how can you, an amateur, possibly hope for long-term better than average, against all these well-funded, well-researched teams?

Seriously, grab yourself a copy of A Random Walk Down Wall Street. I'm not strictly efficient marketeer, I do believe there's some loose change left for the truly enterprising, but I have some perspective: I am not the next Buffett. Neither are you. If you're beating the S&P, chalk it up to recency bias. Check back in in 30 years.

2k a month investible income is super solid. Also, don't compare to others and don't be envious of parental handouts --- read The Millionaire Next Door --- children who receive substantial parental hand outs are generally not good at saving. If you can keep this rate of savings and returns of 7%, you'll be a millionaire in 20 years. Living on your own and saving 2000$-2500$/month is super solid -- the median single income in Canada as of 2012 was 37000$ or something like that, so you're definitely above average.

Steps 1-2-3-5 look solid. a 10k emergency fund is pretty substantial --- that's an instantaneous decent used car, any dental or medical emergency relevant (but my guess is your employer has a decent policy). You might want to consider a 5-8k emergency fund, depending on monthly expenses and your jobs stability.

(Don't purchase another swiss watch. One is plenty :P )

CCP says ETF for 50k+ on premise of charges for fund purchases, a problem that Questrade solves.

1) As long as you're doing it with Questrade, monthly or lump sums as you like. Monthly is technically better, as long as you're good at ignoring any market swings when you look at your portfolio and rebalance.

2) After TFSA, RRSP or non-tax sheltered fund with your bank (presumably Tangerine?) and in the exact same index funds. RRSP is better if you have higher income now and lower income in retirement. I'm guessing your income now and in retirement, but your RRSP is probably good.

3) Not sure on this one.

The best thing for you to do is to read a book about investing. I recommend A Random Walk Down Wall Street; it's very readable and sensible. A little bit of thorough knowledge (sounds like an oxymoron but it's not) will set you up for a lifetime of good investing. Do not piece together what you know from reddit comments and moneysense articles. Don't be in a hurry with your 10 g's.

Planet money did an episode on this week an American focus. Essentially implementing this system in the US was halted due to certain lawmakers wanting taxes to be a huge pain so that people would see then as a burden. Small government etc. https://www.npr.org/sections/money/2017/03/22/521132960/episode-760-tax-hero

Why not get a Multi-Currency Account from Wise? It would literally solve your issue, it's built for people who work for companies based in another country than the one they live in. You will get a bank routing number that's local to your employer if they're based in the US, UK, EU and several other jurisdictions.

The account itself is free and Wise's FX rates are going to be better than the bank's.

https://wise.com/ca/multi-currency-account/

You can then transfer your funds from your Wise account to your bank account for a low fee.

Hey, it's me again! :)

I am just going to reply here so you see it. I think your budget is good, obviously as you can see from the replies, most people think you are a touch on the frugal side for some things, but if the amounts you budgeted work for you, then that's great! Have at it.

I went through my own budget to see if there was anything there that hasn't been mentioned already, I've been tracking my spending for over a year so I feel like I have most things covered, the things you might want to include:

- Haircuts?

- Health Costs (Dental, prescriptions)?

- Gifts (Do you buy anyone birthday gifts or maybe save from Christamas gifts)?

- Sports or working out?

Other than that you seem to have most things covered. You should try to get into the habit of tracking your spending, then you can adjust your budget accordingly when you get a better idea of what exactly you are spending. I use YNAB to track all my spending, I love it, it has saved me so much money just by making me think before I spend, also it's Free for Students! Theres a subreddit for it where you can get help on using the software too.

Congrats on being on top of your finances! Hit me up if you have any questions.

I can't recommend "You Need A Budget" enough. https://www.youneedabudget.com/

Many budgets look at what you are going to make, and you spend dollars that you may or may not have, and you hope the paycheque comes in to cover it. This program sets you up so that you are actually spending this pay period what you made last pay period. So you have specific amounts that correspond to actual dollars that you have. If you overspend in one area, you have less to allocate next period.

It turns "well, you should spend this much in these areas" into "This is what you have to spend in these areas" and really helps avoid the abstractness that made normal budgeting easy to fudge for me. There are consequences when you overspend, because it directly carries over into next month's budget.

It also encourages you to "budget" for long term expenses. For instance, we have budget items for car repairs and yearly memberships and similar large irregular expenses. You save a little each month so that when the expense comes you have the money, rather than trying to find where you're going to find it.

The whole program is about not spending money that you don't physically have. It weaned us off of credit very nicely and brought us to a point where we have a nice emergency fund and few debt expenses.

The program itself is very useful, but the concept of the YNAB budget is the really valuable thing.

For the asbestos, watch out for visible items that are PACM (possible asbestos containing materials). Asbestos containing fibreboard and duct tape are commonly found on HVAC ductwork and around vents of forced air systems. They are both white in colour and are know to contain high content, chrysotile asbestos.

Vermiculite is another item that should be watched for and most home inspectors will be able to identify this without issue. Vermiculite will often be found in the attic but can migrate down into walls and voids. The characteristic shiny mica pieces can contain asbestos but not always. It will sometimes falls down into light fixtures and on other flat surfaces like the top of cabinets so watch out for pieces of debris.

Vermiculite whether it contains asbestos or not is a black eye on the home given the dangers associated with friable asbestos. Testing can be done to confirm the asbestos but it's quite costly and in the end, may be an expensive way to learn there is asbestos.

If you are looking to learn more about asbestos in real estate transactions please read my ebook it's free for Amazon Kindle Unlimited members or a low cost educational guide for non-members.

https://www.amazon.ca/Asbestos-Exposed-definitive-identification-including-ebook/dp/B08H2KS528

Great points to emphasize. Highly recommend Aegis for Android. I have it set to backup my tokens occasionally to a NAS on our network. Zero cloud involvement.

They're two totally different styles of books. The first is a narrative (basically a Canadian reimagining of Clason's The Richest Man in Babylon, covering many of the same points). The second is basically just a bunch of chapters on different topics.

Sure, the investing advice in the first book is outdated, but the personal finance aspects of it are not. I personally think the first book is a lot more valuable than the second one pedagogically.

So, I shouldn't comment on your specific financial questions, but I can address the topic of psychology somewhat. I will say that when people who have encountered severe psychological distress / events look back on their life, the ones who survive are the ones who are best able to reframe the experience.

I suggest you specifically read the work of Viktor Frankl, the Austrian psychiatrist who survived the holocaust and is one of the leading thinkers on humanity's darkess moments - and our ability to survive them. This is not something to take lightly, and based on my own personal experience I think you might benefit.

His book is readily available, and is called "Man's Search for Meaning."

Send me a private message with your address and I'll send you a copy.

Cheers

Before you do anything I suggest doing some reading first.

My suggestions are:

Millionaire Teacher: The Nine Rules of Wealth You Should Have Learned in School.

The Wealthy Barber Returns.

The Little Book of Common Sense Investing.

From that point check out Canadian Couch Potato. Specifically he has created 3 model portfolios that should be relatively easy for you to setup. Option 1 being easiest and option 3 being the hardest of the 3.

Within each of the 3 model portfolios, he provides several different asset weightings so you can choose how conservative or aggressive you want to be with your investment. Each model also lists the MER you'll be paying, and they are all way cheaper than the 2.47% you're paying now.

My suggestion to you?

Sell your CIBC mutual fund portfolio asap.

Open an account with Tangerine and use the CCP model 1 portfolio.

Continue reading what I suggested and learn more about your personal finances.

Check out the sidebar on this subreddit and /r/personalfinance to find more material to read and learn about your personal finances.

Once you feel more comfortable with investing look into moving your funds from Tangerine into either the CCP model 2 portfolio with TD Waterhouse and the e-series funds, or get your hands dirty with model 3.

EDIT Just a quick note. OP don't get down on yourself about this. I made almost the exact same mistake as you when I started out. I bought into a fund with a 2.20% MER, and I held it for 6 months before I realised my mistakes. Just recognize that you can be doing better and start doing it.

Stop Over-Thinking Your Money, by Preet Banerjee is another Canadian one. Much of it will re-tread ground covered by Millionaire Teacher, but the insurance/disaster-proofing your life chapter is worth a read.

The Value of Simple, by I don't know, just some guy I guess, focuses on index investing and how you actually do it in Canada.

MoneySense magazine has produced a few "guides to X" over the years, the most notable of which is the MoneySense Guide to the Perfect Portfolio by Dan Bortolotti, which is more on index investing (focusing more on the whats and whys than the hows of VoS).

Looking beyond Canada-specific stuff, Carl Richards just came out with a book called The One-Page Financial Plan which looks promising (but I have not yet read it myself), and another I have yet to read is Happy Money by Dunn & Norton. I quite liked Dan Ariely's stuff on behavioural finance, especially the part on how different we consider things that are free in Predictably Irrational. The Little Book of Common-Sense Investing by John Bogle is a good read on the concept of index investing, but the examples are all US-centric.

Millionaire Next Door comes out of the US and is not specific to Canada (as you can tell from the subtitle).

I use Koho for my weekly miscellaneous spending/saving and I love it.

I've found creating a budget easiest if I have line items for recurring expenses, and then one bucket for "everything else".

I used to use cash for this, but it's way easier with Koho. Every Monday I send $X to it and that's how much I have to spend/save for the week.

E-transfer deposits are free (in the memo record what your bank is charging you and they will reimburse you)

Their roadmap is public so you can see what they are working on https://trello.com/b/Qz5nPnOb/koho-roadmap

Edit: I should add that it's the UX I appreciate most. Especially saving for goals. If I want a $300 something I just set a goal and when it's done I can buy it.

I have Delonghi ESAM 3300 , I pour beans in the hopper and all my coffees are Americano, takes ~30 seconds. The only downside is that it’s so easy that I would drink way too much coffee when I first got it. I got mine used and changed a handful of o-rings, they’re remarkably simple to repair. My sister has a Miele and loves it.

> I think that is why Costco is so successful. People readily believe that since they are buying in bulk that they must be saving money overall. But I have found that is simply not the case.

Odds are that you probably are saving money by buying at Costco because they can afford to have lower margins and pass the savings on to you.

Costco had US$ 3.2B in operating profit, and membership revenue was $2.4B. Given that membership revenue has almost zero overhead, that means subscriber fees make up 75% of earnings.

If they've made a dollar off of you before you even enter the door, why bother gouging you once you're inside? They could have zero margin on every item they sell and still make a profit.

- https://www.fool.com/investing/general/2015/06/10/why-membership-fees-are-so-important-to-costco-who.aspx

- https://www.reuters.com/article/us-costco-wholesale-results/costcos-profit-boosted-by-higher-membership-fees-strong-u-s-sales-idUSKBN18L2QR

So is it any surprise that they don't bother trying to squeeze every last penny at the cash register? Since you've already given them (most of) their profits, might as well make it up by getting discounts on the items.

>Downside is the cost which is getting a bit high.

Agreed. I'll still use it though.

They have a free trial for 34 days going on right now: https://www.youneedabudget.com/. Sadly it used to be 4 months.

You can use Wave Accounting for free to keep track of your income and expenses. https://www.waveapps.com/accounting/

You can file your taxes yourself, Simple Tax makes it really easy because they give you a break down of things to write off. Simple Tax is also by donation. T2125 Statement of Business Affairs is the form you want to use. http://simpletax.ca

This was the one I ordered (From Amazon):

Tojiro DP Santoku 6.7"

https://www.amazon.ca/gp/product/B000UAPQEA/ref=ppx_yo_dt_b_asin_title_o03_s00?ie=UTF8&psc=1

I spent a lot of time on /r/chefknives and trying to determine where to buy. No regrets at all. It's a little shorter than my previous one, but it hasn't been an issue at all.

It's this one: https://www.amazon.ca/gp/cobrandcard/marketing.html

Right?

It looks like the US one has some problems based on the reviews. Canadian one doesn't show reviews but it looks good! I travel a lot so that card would be useful.

I tend to like to use cash when I travel though; could I use the Amazon Visa card to get cash advances at ATMs?

> I'd recommend A Random Walk Down Wall Street, written by Burton Gordon Malkiel.

> > Yup this is a great read!

I mean, I read a lot, and am very interested in personal finance, and I found it super boring. His outcomes are summarized much more briefly by many others.

OP for Canadian book look at wealthing like rabbits if you want something super introductory. It's great.

A Random Walk Down Wall Street by Burton Malkiel is all about this. It’s much more technical than the books you’ve mentioned, but it persuasively teaches the key point about discipline: you can’t time the market, and if you try you are likely to lessen your returns.

You're broke. The sooner you accept it, the easier the coming required changes will be. I recommend you spend a few hours reading Total Money Makeover by Dave Ramsey. He's been helping a lot of people to get out of situations like yours for 25 years.

Right away, things that you can address right now:

- Get rid of all those subs. You can't afford them.

- Eating out, that's over too

- Not sure what kind of car you own, but it's killing you. You need to sell it and get a beater while you get out of debt

- If you can, do overtime at work. Otherwise get a second job.

- List your debts from smallest to largest: pay them in that order

- Time to Kijiji a lot of the stuff you own

It's not going to be easy. Your life will suck for a year or two. But you can do it.

Also, getting in this much debt means you're terrible with money. I'm guessing you're trying to keep up with the Joneses. Unless you change your behaviour, you'll crawl under debt again soon. Time to learn about personal finance.

Good luck!

I'm assuming you're tracking your spending?

I did the exercises in the book "Your Money or Your Life" and the one that was the most powerful was looking at the monthly totals asking myself series of questions on each category (housing, food, entertainment, etc.). The gist of the questions was to help you determine if working to pay for each of these categories was worth it to you. To be honest, the first month, all the money spent in each category was justified. The second month, every thing was justified, but spending $xx on magazines wasn't justified considering I hadn't read the ones from the previous month. That was it on buying magazines after that. My spending went to near zero except for specific crafting magazines.

And so on. Eventually, some categories never changed (housing, for example) but others were scrutinized more deeply, and I would ask myself why I was still spending $xx every month, and issues came up about mindless spending that I hadn't been aware of. One particular category took 5 months before it started going down, so these exercises are for the long run if you want to see any permanent change. However, if you stick with it, you'll give up some expenses willingly, which is a whole different ball game than if you quit cold turkey because you think you should. There's nothing like feeling deprived to get back to where you were.

No matter how well-researched your stock picks, risk will be higher because you'll be less diversified. If you were very careful, on average, your returns may be similar to the overall market. However your risk-adjusted returns will be lower, since your risk will be much higher. Essentially, you take on additional risk without being compensated for doing so. That is to say, that you have mathematically little to gain, and a lot to lose, by using individual stocks. Holding a dozen blue chips was how previous generations invested, mostly because ETFs didn't exist. I'll take boring any day. If you'd like to trade stocks, set aside 5% of your portfolio for this purpose. If you beat the market for a year, or five, just remember that you almost certainly don't have a gift, but you were lucky and your performance will eventually mean-revert. So, don't be tempted to expand beyond the 5% ;)

Recommended reading: A Random Walk Down Wall Street

This^. I cannot stress this enough. Look at your future employment prospects. If there are none because you're majoring in something like Mediaeval French Literature or Gender Studies - GET OUT. NOW. Do not piss away another semester. If you enjoy studying that subject, then you're in luck - you were born into the Information Age and you have unlimited resources to study that to your heart's content - for free! Do NOT throw away four years of earning potential and a ton of otherwise useful money just to get a nice piece of paper to hang on your wall.

You can have a BA, MA, PhD, MSC, ABC, but if you don't have a J-O-B...it doesn't mean much.

Unfortunately you do not get to decide which career paths pay well - the market does. Make sure you pick something that will give you skills to fill a market niche and make some cash. Poverty sucks.

Earn more than you spend, and start developing good habits. EDUCATE YOURSELF. Read The Richest Man in Babylon. Sock away 10% of all your income and invest it in something that will grow.

Educate yourself in personal finance (you do NOT have to pay anyone to do this, remember - we live in the Information Age, knowledge is free and plentiful). Learn as much as you can. Knowledge pays the best dividends. People who know how money functions make a lot more of it than those who choose to remain ignorant.

https://www.schwab.com/resource-center/insights/content/why-own-bonds-when-yields-are-so-low

> Key Points Investors should still consider holding bonds, even though yields are still near all-time lows.

> High-quality bond investments can still provide diversification benefits, and there’s a cost to waiting for rates to rise.

> Bond ladders can help investors stay invested in the bond market regardless of the interest rate environment.

Be on CDN payroll with CDN deductions for tax, CPP and EI as per the regulations for CDN employees. They could use a payroll service if they don't have CDN operations.

If they don't follow the rules and put her on US payroll, she will file 2 tax returns (US and Canada). She will eta. W-2 for the US income and since she isn't working int he US, she will have her tax and FICA refunded. She then converts the US income to CDN dollars using he Bank of Canada average annual exchange rate. The income is foreign income.

1) yes you have to open a US bank account for simplicity (TD and RBC are the main cross border account solutions) and use Wise.com to transfer money to Canada. She may be able to use wise.com for regular payroll as well.

2) Earned income increases RRSP contribution room.

You mean your RRSP withdrawals? Because if you didn't do that, you'd have some savings for retirement and also less of a tax bill.

To me, this situation of not making ends meet without this withdrawal really sends a signal that there is a budget issue. Finding $1,000.00 in a budget isn't hard if you know where your dollars are going, and have a reasonable plan to address it.

What you have to think about here, beyond the tax situation, is that your RRSP is meant to grow so you can retire with it. Compound interest takes a ton of time to start working for you, and you are essentially resetting the clock every time you dip into the account.

Just to add, I am not the only one that's saying this to you; sure maybe your question didn't necessarily deal with your budget, but your budget is a financial tool to secure your lifestyle now, and in the future. You would do well to consider all the advice you're getting about budgeting.

I highly recommend YNAB (https://www.youneedabudget.com/) - not a course, it's a program/app that is basically an electronic version of the jar method for budgeting. You learn to deal with the money you have on hand and actively choose where to spend it before it gets spent. It makes you incredibly aware of where the leaks are in your current spending habits, and I've found it works wonders in improving those habits.

yes and no,

yes if go with latest hype,

do really need a bike, with nasa tech and carbon so can lift with one finger ? back in day we got bike which look solid enough to survive the first ride,.

do really need an apple watch and iphone Pro with data-cellphone plan and apple music subscription ?

for video game, do wanna a AAA game with hyper-real graphics with take 300 artist to create ? you could get a cool and fun indie game for few bucks instead ? (like gog.com)

do lastest camera with 50 megapixels ? incase if u want wall print of crppy picture... or instead get a killer camera used from 5 years ago for few bucks...

etc etc.

I used both FreeCodeCamp and The Odin Project to get an idea if I liked programming. Both are great but I found ToP more engaging and easier to stick to.

But if you want to dive in quickly and get you're feet wet FCC gets you writing HTML within minutes of signing up.

If at all possible let them say the 1st number. 50/50 chances its higher than what you would have said. Come in prepared with information in your back pocket in case ( https://about.gitlab.com/handbook/total-rewards/compensation/compensation-calculator/calculator/ ) Gitlab publishes numbers adjusted for location, so find a similar job and get the high and low. Keep in mind those are salary numbers, if you work as a contractor, you have to add a good margin to account for EPP, taxes, etc, etc. Rule of thumb? Whatever you think is a low/reasonable rate... double that and you're in the ballpark.

Also salary is nice, but its not all. Make sure you talk about everything else as it relates to working conditions ( vacations, training, conventions you want to attend, certifications, insurance, etc)

I'd like to suggest having a budget and sticking to it. YNAB is great for this - assign each dollar a job and stick to it.

Also, use this spending flowchart to prioritize your spending. As a new grad, it's too easy to be overwhelmed with "I can afford that" with regards to monthly payments (new car, new things, vacations, etc) when it really should be... I can save for that (and pay it off in cash).

{kind=link}

Keep paying more than your minimums each month and you'll be out of debt soon enough. If you want budgeting help, this sub is great at it as well. It's helped me a ton too!

Best of luck!

Mint had an infographic about pet ownership a few years back. Granted it was based around spending patterns for Americans, but it may give you a broad idea of what to expect.

Since your Shiba Inu is over 25 pounds, I believe it qualifies as a medium dog, which Mint users are spending an average of $695/year.

- 34% recurring medical

- 32% health insurance

- 17% food

- 8% toys/treats

- 6% misc

- 2% license

There was also this article by Kiplinger. I like it since it breaks down various expenses you can expect. It also brings up grooming and travel care which is something that isn't covered by the Mint infographic. They estimate a medium dog will cost $955/year. Plus some initial upfront costs for supplies (leash, collar, bed, water bowl, etc).

There are ways to do toys and supplies frugally so it is definitely possible to get these numbers down.

I would recommend getting your kitty used to pine pellet litter from the get-go. I initially switched because my cat has a ton of allergies, but it is SO ridiculously cheap, and clean compared to regular litters.

You will need a sifting litter box, which is not a huge expense. A 40lb bag of the pellets will run you around $7 and it will last you about 6 months. When the litter gets wet it turns to saw dust. I then empty this into yard waste bags on garbage day.

Here is the link to pine pellets and the litter box I am using: https://www.canadiantire.ca/en/pdp/softwood-pellets-40-lb-0642778p.html https://www.amazon.ca/Van-Ness-CP5-Sifting-Assorted/dp/B0002ASCO4/ref=sr_1_5?dchild=1&keywords=sifting+litter+box&qid=1624193412&sr=8-5

I also recommend shopping around for a good vet. My cat has had a ton of different vets because of her allergies, and moving around a lot. She is my first pet, and I didn't realize the costs and treatment varies so much between vets. A local facebook group is a good place for recs.

Pre-emptive congrats on your new little family member. They are a joy :)

You don't need the land line.

You can get a VOIP phone number for less than $2/mo at voip.ms, then get a device like this one to connect an analog device like a cordless phone or your alarm system. As far as the device is concerned, it has a normal landline.

Pay for:

- Just internet: $40-$60/mo with resellers like TekSavvy

- Voip line: $2/mo

- 2-3 streaming services: ~$30/mo

Now your total has gone from $280/mo to under $100/mo.

I second NordVPN, I got it for $70 for two years. I'm currently using it to watch It's Always Sunny in Philadelphia, which is available on UK Netflix right now. It also works on my phone and table too.

I have an Apple TV and find it pretty good. With an extra bluetooth controller such as from Madkatz it is fun to play games on .. granted the audience is 7 years old. Supports Crackle, amazon, Netflix, and pretty broad connections with content and apps from CBC radio, TV. The voice search is natural and keeps getting better. I have seen sports channels but don't watch that sort of thing. CBC will show me news from any town in the country, as well as the National, on demand.

I have cable internet and NordVPN and that's it.

I have the TV (and a laptop) connected to a ceiling-hung projector, which decodes audio out of the HDMI and sends it down a 3.5mm cable to a Marantz stereo and posh speakers that I found on craigslist for a bargain. I could get good TV on the air here in Toronto but just don't. We mainly watch movies.

Have you tried a TV antenna? What can you get?

​

Bill Bernstein's The Four Pillars of Investing is another great one. I agree that emphasizing 'in Canada' needn't be a first step, more of a last one just in terms of "how to implement" the wisdom you get from a broader base of knowledge. OP's already got Graham and Bogle on his reading list, so I'd say he's off to a good start.

I can share the contents of my finance section. Wealthy Barber Returns - a bit too basic for me, and I'd wager you too. Millionaire Teacher - my favourite novice book I lend to anyone interested. Somehow makes investing into a real page-turner topic.

Passive investing: A Random Walk Down Wall Street (meaty but approachable comprehensive exploration of passivity). Seeking Alpha, and Incredible Vanishing Alpha (exploration of why alpha is becoming harder to achieve as time passes). I also just snagged a John Bogle title - the guy is a legend and practically a hero to the little guy investor.

Broader scope: Four Pillars of Investing. - Sticks to passivity but goes all fancy with portfolios. Dives into the math a bit further. Good market history coverage too.

Stock picking: Intelligent Investor - heavy slog through the mind of a master. One Up on Wall Street - similar theme and approach but a bit more modern and approachable, from a guy with a hell of a record managing a mutual fund. Both are somewhat out of date but still interesting.

Comedy: Where are the Customer's Yachts? A roast of wall street, from many years ago but still remarkably relevant.

A way to control my spending without the feeling of being deprived kicking in. Think of being on a diet, except with your wallet! Reading the book "Your Money or Your Life" and doing the exercises changed my perspective. Now it's the other way around. I'm more likely to say no to spending money.

A good book that could help you get out of debt is Total Money Makeover by Dave Ramsey. It will guide you through a process that has helped thousands of people get out of debt. I highly recommend it.

The gist of it is:

- Write down your budget and track your expenses. You need to know where your money goes. Every cent.

- Save 1000$ as a initial emergency fund.

- Get current with your debt payments. Then list all your debts from smaller to larger, and pay them back one by one starting with the smaller one. Some people here will say you should pay the one with the highest interest rate first. Personally, I prefer Ramsey's method. Because once you start getting rid of debts, you'll start feeling good about yourself.

- Save up 3-6 months of expenses in your emergency fund.

- Start investing money towards your retirement.

- And then ultimately, you would start paying your mortgage back ASAP. But you don't have one of those yet.

And once you're ready to get serious about investing for your retirement, I suggest you read Millionaire Teacher.

Time is running out, so I think you're probably smart to shelter cash in an RRSP ASAP. I wouldn't keep it sitting around for 6 months though. Get your investing education started sooner than later. Be sure you won't bring your tax rate down too far though - eg. contributing most of your years' earnings. Might make sense to use both TFSA and RRSP savings accounts to bring the tax rate down to a reasonable level but not any further.

I'm a real believer in indexing, so I'm going to tell you to start with Millionaire Teacher. Then, move on to A Random Walk Down Wall Street. Then, hit up the Canadian Couch Potato blog and spend as much time there as you can. Finally, pick a model portfolio, implement it as cheaply as possible (Questrade+ETFs is looking pretty good to me for someone with lots of seed money and contributing regularly). I bet you can do all of this within a couple of months. If you're reading lots and listening to podcasts, I'm betting you're going to be a DIYer, and a robo-advisor probably isn't the right fit for you. Remember, it's not rocket science, index investing is really very simple (couch potato being a very fitting name)

The Millionaire Next Door: The Surprising Secrets of America's Wealthy

It's not specific advice like the Barber, but I found it very interesting. Also by the same author, Stop Acting Rich: ...And Start Living Like A Real Millionaire

As a complete newcomer to investing I found these all to be really useful. Focus for all is on index investing.

A Random Walk Down Wall Street (book) Moneysense (magazine)

Canadian Couch Potato http://canadiancouchpotato.com

> Is there any way to get more comparison data? Optimally, it'd be cool to say "If I'd done this 5 years ago, I'd be here right now, instead of where I am today"...

GlobeFund and Morningstar may provide more numbers for comparison. But the main point you need to understand is that for actively managed funds there is a huge amount of evidence that past performance is a bad indicator of future performance. The best known indicator of future performance is the funds fees, with the higher the fees the worse the performance.

So while it's common for many funds to have a few good years where they outperform the market, it's much less common for them to keep this up for 10 or 15 years.

You may want to do a bit more reading of the theory of passive indexing and why the math so rarely works in favour of active management in the long term. The Millionaire Teacher is a good starting book and will go into more detail than you can find on the CCP website. It's also written by a Canadian and covers Canadian concepts.

If you want more theory, you could read A Random Walk Down Wall Street and The Four Pillars of Investing. A Random Walk is not that difficult a read. While The Four Pillars can be a tough slog for some people, especially if you don't like math. Although if you are from a coding background, I don't think the math should be that bad.

.

And before making the decision to involve a fee based FA, you may want to do some of the reading first. After doing the reading you may still find that a fee based advisor is the way to go and there is nothing wrong with that. But it sounds like you may be more confident of your choice if you have a better understanding of some of the background first.

Your thinking of Barber, not Butcher. :)

Anyway, The Wealthy Barber Returns is a good introductory book on the basics of personal finance. So investing is part of personal finance, but the book also cover many other areas of personal finance. The original Wealthy Barber can be hard to find since it's out of print, but it covers roughly the same topics Wealthy Barber Returns. The author did however slightly update his recommendations in the new book.

The Intelligent Investor is considered a classic in value investing. This is a type of investing where you spend a lot of time studying the annual reports and financials of companies, trying to find stocks that you believed are undervalued. So this is a different type of investing than passive indexing and if you aren't going to index, it might be the best method. But most people would probably be better off sticking with passive indexing.

If you are looking for more theory on passive indexing you could check out A Random Walk Down Wall Street and The Four Pillars of Investing. Both are considered classics. A Random Walk is definitely the easier of the two to read.

Many people find the math behind The Four Pillars to be a bit complex. But it should be noted the author actually simplified the math in Four Pillars compared to his previous books, as the level of math in his previous books scared off a lot of people.

Start by reading this article: http://bucks.blogs.nytimes.com/2013/06/11/what-you-dont-know-about-your-portfolio-may-help-you/?_r=0

I would encourage you to read books like "Millionaire Teacher" and "The Four Pillars of Investing" to assuage your fears about "the economy."

Jump in. Set your asset allocation, select low-MER funds that fit with your asset allocation, then never look at your portfolio except on your annual (semi-annual? quarterly?) rebalancing date.

There's an analogy I'm fond of:

> Investor Ralph Wagoner once explained how markets work, recalled by Bill Bernstein: “He likens the market to an excitable dog on a very long leash in New York City, darting randomly in every direction. The dog’s owner is walking from Columbus Circle, through Central Park, to the Metropolitan Museum. At any one moment, there is no predicting which way the pooch will lurch. But in the long run, you know he’s heading northeast at an average speed of three miles per hour. What is astonishing is that almost all of the market players, big and small, seem to have their eye on the dog, and not the owner.”

If you're watching your investments or "the market" you're watching a schizo dog. The owner is steadily moving in one direction. (~7%/year over the last 100-years). It could be down 10% in one year, up 200% in the next, but it'll average 7%.

Stop watching the dog.

> Specifically, if you review the 5 year returns of actively managed funds VS the Index you will find that actively managed funds have outperformed the index.

I did look at 5 year returns. And for the 5 years ending in 2011, the percentage of actively managed Canadian equity funds that beat the index is 2.75%. That's it. Meaning that 97.25% of actively managed Canadian equity funds didn't beat the market. And that's pathetic.

The research is exceptionally clear. Over long periods the amount of actively managed funds that will bear the index is extremely small. You can read A Random Walk Down Wall Street if you want a review of all of the academic literature.

And yes, a small number of funds will beat the market. But the problem is that it is nearly impossible to pick them out in advance. The research is also quite clear that funds the outperform in the past have a greater than average chance of underperforming in the next time frame.

> If it were clear cut "Active or Passive is better" there wouldn't be so many Active investors getting paid such large amounts.

It's mainly just marketing. Large number of investors are ignorant and want to believe they can pick the manager that will outperform. And they'll pay big bucks to take the chance. And even when it doesn't work out, they'll continue to pay the big bucks, because they figure soon they'll pick a manager who'll get it right.

> If you put you wallet or purse on the counter

This is extremely unlikely. In the best case with those in store readers you might get 10cm. Typically you'd get less.

If you'd like to try it, next purchase hold the card a couple cm from the reader and see if it will work.

The more interesting issue with tap is that I can walk by you at the mall and read your CC number out of your wallet/purse.

If you want to see what the card returns then install an app on your phone and scan your own card.

The street is betting the US Fed will not raise rates as planned. USD selling off a bit, which generally means risk on for other things. So, USD is weakening relative to CAD.

Here, check the 5 year on US Dollar Index (DXY) and where has the trend been: http://www.marketwatch.com/investing/Index/DXY?countrycode=US

Now, the question is what catalysts will bounce it back the other way or if we've hit the end of the trend.

Warren Buffet said of dividends, " I must have been in the bathroom when the decision was made."