What are

/r/leanfire's

favorite Products & Services?

From 3.5 billion Reddit comments

The most popular Products mentioned in /r/leanfire:

The most popular Services mentioned in /r/leanfire:

Schwab

Cronometer

Meetup

You Need A Budget

craigslist

The Motley Fool

Healthcare.gov

Udemy

Worldometers

IMDb

SlingPlayer

Rasterbator

Preply

Wallet App

NPR News

The most popular Android Apps mentioned in /r/leanfire:

7 Minute Workout

GnuCash

ClockworkMod Tether (no root)

Goodbudget: Budget & Finance

The most popular reviews in /r/leanfire:

Left behind how? You have approximately $15,000 more than the average person living in the wealthiest country in recorded history. That's about 6 months of savings for you (or more). From a financial standpoint, you are certainly not "behind." I wish I made $32,000/yr at age 21.

With regards to friends and dating and socializing, I think that's where you may find it valuable to devote more attention. There are plenty of resources to help you become more social. You can devote time to journaling and introspection and meditation to help you address your anxiety; you can read How to Win Friends and Influence People and other classic self-improvement books; you can make friends online in various forums and practice becoming more vulnerable with them, etc.

Treat it like any other life skill you want to cultivate. There are ways to reliably make more money, become more emotionally intelligent, master a sport, earn an advanced degree, and so on. Becoming social and engaging is just another skill like those.

Meal prep. I regret not getting into it sooner, as it has saved me lots of money, and most importantly, it has saved me tons of time.

My gf and I purchased a 15 pack of microwaveable storage containers (like these for example) and once a week, i'll cook up a large enough meal to last the work week and will divvy out the food into the food storage and keep about 2 days worth in the fridge and the rest in the freezer. Usually, we'll fill the smaller compartments with rice or mashed potatoes or frozen vegetables that we buy at Costco in bulk and the main compartment will have something like chicken alfredo, pulled pork, curry, ribs, stir fry, etc. Prep is mostly passive (oven or slow cooker) and at most takes ~2-3 hours out of my saturday. Each meal comes out around $2-3 a meal and is ready to go after a couple minutes in the microwave and then all trays are dishwasher safe.

Look up cohousing. Especially ones that remodeled existing structures (like N Street Cohousing) rather than building new. Creating Cohousing is a great book to read on it-my local library has a copy, but it's on Amazon here: https://www.amazon.com/Creating-Cohousing-Building-Sustainable-Communities/dp/0865716722

I have just started my journey into the fascinating world of FIRE. It started a couple of weeks when I finally decided to sort out my finance. I have been procrastinating for so long I'm now kicking myself for not having started earlier.

I went from being nearly totally ignorant about personal finance and the possibility of becoming financially independent and retire early and keeping large amount of savings in a nearly 0% return saving account to:

1. Getting myself acquainted with FIRE basic concepts ("Can I actually retire early? Why nobody ever told me that!")

2. Define an investment strategy possibly leading to FIRE, including getting familiar with ETFs and asset allocation concepts. The Bogleheads Guide to Investing was a good reading, though I was already familiar with most of the concepts thanks to several subs on Reddit;

3. Select a low-cost broker and open an account with them;

4. Make my first deposit and first investment;

5. Set up a monthly budget spreadsheet on Google sheet, to help me get an overview of my monthly income/expenses, and identify potential further savings. It will come in handy when I will start making projections about my target retirement age/spending.

I'm very happy how things turned out! I finally feel I'm in control now.

Just keep remembering, consistently save. I didn't start saving until well after your age and it can be done.

What is important is not how much you have saved, but building a plan (or plans) and save each month. Each month you will feel better that you have paid yourself.

Careers take time. You have hardly lived. Two people, two incomes?

Read all of the early retirement books. Read Your Money or Your Life. Keep updating your financial plans and live your life today. We can't live for tomorrow.

Keep busy, keep achieving. Just remember one day you will have enough money to quit your job.

If you know 10 basic functions, you can make a massive impact on most organizations (INDEX, MATCH, VLOOKUP, etc.). I built my career in technology exactly this way; my company was looking for a way to predict which sales regions were most likely to grow the next fiscal year. I built some coefficient tables and PivotCharts over the course of a week, and, a year later, I had a role in technology operations. Today, I work at a top technology company, having spent the previous decade refining my Excel skills and picking up new skills (Salesforce, SQL, business analytics).

It's so, so important to understand how to wrangle data if you want to make an impact. Excel is a great first tool to learn. Here's a great resource if you're new to Excel.

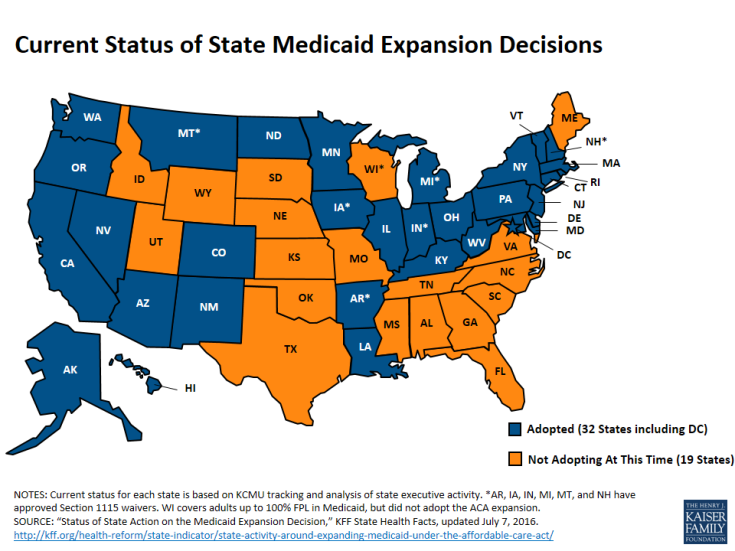

This is a difficult question to answer because it depends on a lot of factors including (but not limited to): what state you are in, what happens to the ACA, how much you plan on living on, and where that is stored.

(Note the username, it is possible everything I know is wrong.)

First, what state you live in, ideally, you want to live ins at state that has expanded medicaid, giving you that option if you are working with an income under 138% of the Federal Poverty Level. This is impacted by how you store your money. (If you are in an orange state, consider moving)

{kind=link}

Second, what happens to the ACA (Affordable Care Act), for the purpose of this question, let's assume nothing happens to the ACA. If the ACA changes, this whole post could be useless.

Third, how much you plan on living on, if you can keep your income below 138% of federal poverty level, you will qualify for the most assistance.

Last, where you keep your money. Almost every factor of the ACA is based on Income, so money from capital gains in taxable accounts has far less effect on your eligibility than money from a job, 401K, or pension/annuity. (Check this for the thresholds in your state)

It's kinda like Googling "how to be an interesting person." The fact that you need to ask is the problem. I'd read The $100 Startup to get some sample ideas. Ultimately, if I could tell you how to do it, I'd already be doing it and collecting the profits.

"Age 59 and under.

You can withdraw contributions you made to your Roth IRA anytime, tax- and penalty-free. However, you may have to pay taxes and penalties on earnings in your Roth IRA"

Emphasis on EARNINGS.

These books:

So Good They Can't Ignore You

The 4-Hour Workweek

The Power of Less

Deep Work

Read em all and slowly integrate the stuff into your life. They've all got slightly different tacks on the same subject really, but there are all sorts of methods you can apply to get more done in way less time. When you are getting more done in an the first hour at work than you used to do in 8 and working from home, you might as well throw a load of laundry in and then take the afternoon off.

I'm not surprised since teachers are typically frugal. We have veteran teachers who make 6 figures (20+ years of experience) and still drive old beat up clunkers. They still bag their own lunch and take on extra duties, have two jobs, etc... I read The Millionaire Next Door as well.

I've just begun rereading Your Money or Your Life with the intention of doing the things in the book that they suggest like getting a really clear view of what you spend and what you make, and keeping a visible graph on the wall.

I'm beginning a new job hunt because even near barebones I can't get to the savings rate I want, and have some other work problems at my current job.

Picnic at the local park. On my staycations, I always liked to go on a picnic. Pack some sandwiches and fruit and off I go. I would also go for a walk on the trails. It was always so relaxing to putz around the park for an afternoon.

Spotify free for music if you don't mind ads (I don't usually).

Take a class online for free Coursera.com or Edx.com. Youtube class (You have to search and put it together yourself. If you have a few dollars to spare try udemy when they have a sale $11-15. These are always interesting. I'm weird and learning is fun for me.

Meetup.com there is a freebie group in my city that lists a lot of free entertainment. ie. Free yoga classes, free concerts in the area. Maybe see if they have one for your area.

You should read the book The Bogleheads Guide to Investing. It answers all of these questions. The market can wait a week while you read a book and come up with an investment plan that makes sense and fits your risk tolerance.

I started my exercise programme (no gym):

Riding my cruiser to the city Central Market on Saturday (5kg return weight) and then to the liquor store on Sunday (25kg return weight); and

Two circuits of "7 minute workout" in a hydrotherapy pool. ==> https://play.google.com/store/apps/details?id=com.popularapp.sevenmins&hl=en

Lost the weight on /r/keto so now I'm working on my fitness.

This is the root of the problem with the tax code - it's too complex because there's always some visible person that loses when some pet tax deduction gets cut. The invisible cost of having a tax code so complex that people pay to get their taxes done isn't obvious.

They are cutting deductions everywhere. I hope they get rid of the mortgage interest deduction, I'm even fine with scrapping the 401k program. These are all things that benefit upper middle class americans while doing nothing to help the poor. I'm all for getting rid of all the deductions and then just hammering out brackets that make sense.

Tuition wavers are income. So is forgiven debt. If your employer offers it for free, it's part of your pay and letting grad students get paid $50k a year by a school and make it look like $30k a year is unfair. I'm even in support of making all the benefits we get taxable. If that results in an increased tax burden, then lower the rate and then the people at the bottom can benefit too instead of just the people that have $150 to pay to have their taxes done.

What makes economic sense often isn't what's politically popular. You'll love this podcast: https://www.npr.org/sections/money/2012/07/19/157047211/six-policies-economists-love-and-politicians-hate

I wouldn't give up on the language. There's something known as a frequency dictionary. If I recall correctly, a university in the U.S. studied the English language (but generalized their results to other languages), finding that around 85% of everyday speech is only comprised of around 1,000 words (e.g. numbers, days of the week, verbs like eat, sleep, work, etc.), so if you can learn these words and basic grammar, you should be able to get by with general conversations. I learned Spanish and then Portuguese, but in each, my vocabulary is probably only around 2,500 words, but I understand most of the most-frequent words and understand the grammar rules, so I get by fine in most conversations.

edit: parentheses 2nd edit: a frequency dictionary isn't a magic bullet, but it can supplement your other language-learning efforts by helping you to focus on the words that will be most useful.

For most people the majority of their happiness and stress on the job comes from their coworkers and the company they're at.

This is a management book https://www.amazon.com/First-Break-All-Rules-Differently/dp/1531865208 but it does a good job early on explaining what makes a good work environment and what doesn't. It could be what is normal for you is actually horrible.

Once you know what makes a good work environment it can be a bit easier to go job hunting finding the perfect place.

For some it really is a career change. I did that and am grateful for it, but I chose a neighboring career which was a step up. I'm still doing a lot of the old work I was doing. I just like a bit more of a challenge and I find in my new career it's easier to find coworkers who are less toxic, so it's a win-win. I get finding that can be hard though.

Each month, my spending is limited to $2,500 (including rent, utilities, etc). I give myself that in the budget and can allocate it however I want (YNAB FTW) but that's it. All other money goes into savings/investing, so when I get extra income from a side hustle or whatever, I don't change my spending.

In a moment of recklessness, I bought myself this wonderful foot massager (though I have no clue why it's under review from Amazon... I ordered it Tuesday and it just arrived today... weird). It wiped out most of my remaining budget for the month and I now have a whole $29 for the rest of the month. I think it will be a fun challenge to see if I can get by on that for 9 days. I'm stocked up on my food and have a ton of schoolwork to do, so I should be spending most evenings at home with computer and Netflix.

Highly Highly recommend YNAB (no it's not a referral link but PM if you want one) if you're looking for some budgeting tools. There is a cost after the trial (which they will extend for a few weeks longer if you ask), but it completely opened my eyes to places I could cut. That is all after using a gdoc spreadsheet for years that I thought I loved.

RSUs are taxed as income at vesting. There's no reason to hold. It's generally advisable to sell immediately.

> With annual earnings of 110k and 153k in tax deferred, I don't see how you get anywhere close to RMDs big enough to be a tax problem.

I just want to make sure I'm thinking correctly about the math of this. So, first of all, there is the $153k but next year we could add to it and the market could rise a bit such to bring it up to close to $200k. So let's say it's 200k and we put it into the Schwab RMD Calculator.

That shows it, on its own, growing to a max of $968k if nothing but the RMDs are taken out. (Which is possible, because we have enough in our brokerage account to just live off that, probably). That happens when we are 85. The RMD that year would be $75,839. That year we, if we were still both alive, would also be getting about $24k/year in social security benefits. So our income that year would be about $100k just on these two. Subtract $24k for the deduction (and maybe more because we're oldsters then) and we're at $76k.

Now, at what rate will that $75k of RMD going to be taxed? Currently, for Married Filing Jointly, looks like about $50k of it will be in the 12% tax bracket. So that is $6k in taxes.

Of course, us at 88 means the year is 2058, so the standard deduction will have risen quite a lot in 40 years! So maybe we'd pay much less in taxes. Or, perhaps we're at an all time tax low under Trump and it'd cancel out.

There is also the worry that my wife would have to pay Single Filer tax on that $75k RMD. In which case, she'd have to pay $8k+ on her own.

So, my point of all this is: $150k to $200k in tax-deferred accounts can grow quite a bit over the long haul, and then one's RMDs are sizable. I'm just trying to figure if my math is roughly in the zone. It easily could be off or I could not be taking certain things into account.

Use Udemy.com. They are thousand of courses and skills you can learn with $10. They will be some topics you like more for example drone pilot and you can do roof or pipeline inspections. Do you know that oil companies have ROV pilots? The small submarine boats to do subsea pipeline inspections. I was working in Scotland and you know how many kids without university degree earning more than 100k per year, because they are specilized. Also SLB which is a big service company: they have a department for perforation (google what it is on a production well). They need to build the perforation device with explosives. More than 100k

I am saving money to become an electrician. In the UK it is a 5 weeks course and it costs around $3,500. You can do something similar with night college.

Buy your partner a copy of Your Money Or Your Life.

It's never going to work for you to pay them to run your business whilst you retire, because they'll see it as unfair that you're getting money when they're doing all the work.

There are nearly always resentments when you mix business with friends and family, as the reasons are the same as in inheritance disputes. People rationalise things by saying "but we're family" and "I'd do the same for you" or "I need it more". People often rationalise "what's fair" based on their own needs and desires because they don't recognise their own bias.

Your partner is probably going to expect you to carry them in retirement, because they know you're ok for money. They don't see the sacrifices you're making now or their own wasteful spending. I very much suspect your partner wants their cake and to eat it - most people who spend their money on "fun" crap lack the foresight to appreciate how their current spending is costing them the future.

The advice another poster gave is a little advanced for your current situation.

- Get a budget together. The budget needs to be less than 90% of income.

- Get $1000 in savings

- Negotiate your medical bills down if you haven't already (they should take 1/3 to 1/2 of what you owe)

- Start an IBR program on your student loans

- Put up to $2000 in your 2017 Roth IRA (you have until April 2018). If they'll let you, you can just leave the money in the settlement account (Vanguard Federal Money Market Fund) which is pretty similar to a savings account in case you need the money back.

Given your income, that will probably keep you busy until April at least, just come back and ask for some more steps. The investing should wait until you have enough cash around to cover basic emergencies and any high interest debt is paid off.

Some helpful info: The Saver's Credit should give you 50% of the first $2000 you put into a Roth IRA back in your tax refund. So unless you don't have an emergency fund, it's probably worth doing each year. You have until April of the next year to contribute to a Roth IRA. You'll need $1000 to start one with Vanguard.

Reading:

Normally I'd start with something more theoretical and less extreme, but you need money now so you might as well just dive right in: http://earlyretirementextreme.com/day-1-finding-a-place-to-live.html

Then you can read Your Money or Your Life and The Boglehead's Guide to Investing. Get it from your local library.

A

I follow MMM, Frugalwoods, Financially Blonde, and just finished Your Money or Your Life. Without our debt payments, our expenses would only be $20,000. Paid too much for an education. I will look into ways to reducing even more.

Books. Start with books because they are great at giving a broad, consistent overview of a subject. While you can get an overall picture from blogs or a wiki, it's fragmented and will take you more time than if you had just started with a book.

The "required" reading should be something like these books in order:

- Your Money or Your Life

- The Boglehead's Guide to Investing

- Early Retirement Extreme

Those 3 books form the basis for starting out with LeanFire. The last one is a tough read but does a great job of forming a philosophical and practical basis for why exactly you should consider living off of less.

Books are the place to start if you need an overview. Your first step is the library to get a library card if you don't have one. Then the book Your Money or Your Life should be your first read followed by The Bogleheads Guide to Investing (or similar Bogleheads guide). Since you mentioned that you are trying to achieve FI as fast as possible, then I'd read Early Retirement Extreme.

The first book contains the philosophical underpinnings of Financial Independence and explains how to save the money. The second book will teach you how to turn that saved money into income and the third book is a really tough read that explains the nuts and bolts of how to save a huge percentage of your check and get to Financial Independence in 5 years or so.

Then you can come back and ask for any clarification you need. It's not a one-size-fits-all path but we can certainly point you in the right direction.

Good points. At some point you need to pick a number and go with it. It's time vs. money. At some point, you are going to feel you have enough money and you value the time a lot more (which you may value time more because you have enough money).

Weekends, when not working, my wife and I are surprised by how fast time goes. Especially if you sleep in late, your day goes by very quickly. Maybe that's an age thing, I don't know or conditioning at work for long hours of sometimes not a lot going on).

My wife and I are going to roll on Social Security and my pension. Pension will come earlier than SS. So it's a matter of determining how much we need until SS, how much after extra, if we please, and some emergency/unplanned/non-recurring event spending.

At some point we are going to say, "Okay, it feels right to retire." You reach a certain comfort level. And it's not all about money. It's about time. Thinking about how much time you may have and may have healthy and getting around.

I behoove people to read Your Money or Your Life. I've read it a couple of times and I always getting a refreshed/recharged feeling and reminder of how much time is valuable to me and life energy is required to buy something.

Investments are truthfully all around you. The first place to look is places where you can spend today to reduce future spending. Buying the 12 pack of paper towels for a lower unit cost. Buying the cell phone cash instead of having it rolled into 2 years of increased payments. Insulating your house to reduce costs. The touring tires that cost more bit last twice as long. Run the numbers for both options and treat it like a real investment. If it doesn't double your money in 10 years, don't bother (looking at you solar).

Then there's always paying down debt. It's a pretty risk free investment. You can also self insure - cash reserves allow you to skip the insurance for acceptable losses. Over the course of a lifetime, you are highly likely to save money.

While you are correct that the market is historically high, take that with a grain of salt. Lots of people thought just like you kept there money in cash, then watched from the sidelines as they missed a huge bull market. Some of them finally got sick of it and invested right at the top just to watch it sink.

If you are truly risk adverse and don't know how you will react when the market drops, do a 50% bond 50% stock portfolio until you get to live through your first recession with skin in the game.

I highly recommend you read The Bogleheads Guide to Investing. If that doesn't calm your nerves, The Rational Optimist might help. You need a 30 year investing plan and a bubble here or there shouldn't be too problematic.

This will not work, because you are missing inflation here.

Inflation historically has been around 3.22% (https://tinyurl.com/yadx2dpc), add that to your 4% SWR and you will need at least an 7.22% annualized growth rate in the long run.

Only stocks can give you that, the average long term SP500 total return is somewhere around 8.87% (https://tinyurl.com/y7jzt6ft, this is with data since 1870 taken from BigERN's spreadsheet).

To reach FIRE the fastest, simply DCA VTSAX and you're good to go ;)

Congrats! Sling TV has a current promotion of $15 a month. After 2 months, it will raise to $25 a month. It has HGTV in the lineup. You can also share it with 2 other family members. You can split the cost with each other. This can save you considerable money on your TV budget.

Here's a free copy of my book Building Wealth and Being Happy: A Practical Guide to Financial Independence

https://drive.google.com/drive/folders/1Nt1ws9-5t36EkyClCM9gnmj-ujum8gAz?usp=sharing

It's in PDF, Docx, and ePUB.

Here it is on amazon for reference: https://www.amazon.com/dp/B01MXRXM1A

The difference between investing and speculation is mainly a question of risk. I like to think of this in terms of the definition of an investment presented by Graham in "Security Analysis:"

> “An investment operation is one which, on thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

Source: novelinvestor.com has a summary, or you can purchase the entire book on Amazon

"Safety of principal" is the key phrase here. If you can't reasonably be assured that your principal will be protected, you aren't investing, you're speculating. So if you purchase a wide variety of different stocks, such as through an index fund, in order to track the performance of the overall market or maybe a particular industry? Sure. That's investing.

However, if you make very large purchases of an individual company's stock, you can't reasonably guarantee the safety of your principal. You're over-exposed to idiosyncratic risk. For example, maybe you invested in a company with a good product in a growing industry, but the CEO somehow mismanages the company and it goes bankrupt. Now you are speculating. You'd have less exposure to that risk if you were more diversified.

Now, contrary to what a lot of other people will tell you around here, I don't think speculating is inherently bad. It's just riskier. It can potentially be a good way to make greater than expected returns, but you have to understand what you're getting yourself in for, which is the risk of losing your entire principal.

FYI if your phone data plan has unlimited data, you can get an app that will let you use unlimited tether data for free.

I have an unlimited data plan with Sprint but they don't allow any tethering. So I got this $5 tethering app and now use it as my only source of internet on my PC.

With 4G phone service the internet is usually fast enough to stream 480p on Twitch or 720p on Youtube.

I use this app for android, it's very handy and 100% open source. I once reported a small bug to the developer and they fixed it within a couple of days. You can also export the data and import it in the fully fledged desktop version. Highly recommended :)

https://play.google.com/store/apps/details?id=org.gnucash.android

Simply Fidelity, Vanguard, or Schwab index funds. They are cheap (as low as 0.05%). Target retirement age funds cost a pinch more (for auto balancing)

John Bogle's book on investing that anyone can understand. He started index funds.

You can make your own "lazy portfolio" as well that's cheap: https://www.bogleheads.org/wiki/Lazy_portfolios

Interesting. I've been reading a few pages of "A Guide to the Good Life: The Ancient Art of Stoic Joy" every night for awhile now. Voluntary hardship has been mentioned a few times.

I don't know if this counts, but my wife and I will wear sweatpants and hoodies/blankets in our house when it gets cold instead of turning on the heater. I hate the smell of it and almost enjoy testing how resilient I/we can be during the winter. (Lowest temps we usually see are 30s though, lol)

I'd start with the books Your Money and Your Life and then The Bogleheads Guide to Investing. That pretty much forms the foundation of all this. Then work your way through the Early Retirement Extreme book.

Here are some books that helped me rearrange my job to be one that was more enjoyable while also being more productive:

The 4-Hour Workweek

So Good They Can't Ignore You

Time Management for Systems Administrators

The Power of Less

Your Money or Your Life and The Boglehead's Guide to Investing would be what I'd start with. That will give you a good foundation. In the spirit of frugality, get them from your library.

Early Retirement Extreme is also a good book (written by the author of the blog), but it's a more complicated read and is certainly much more extreme than the others. I'd put that one as advanced reading

I think of it as FIRE + Frugality blended into the sauce. I guess it doesn't have to be frugality, per se. It seems like a blended concept and maybe not so easy to discuss. However, the book, "Your Money or Your Life" (check for latest editions updated for modern times - my first copy is first edition), goes over probably the principles here, but focuses on how important is your money to you? How important is your life? Think before you buy something, sort of thing (I need to reread the book).

You could start a micro business. The $100 Startup has a lot of suggestions. The 4 Hour Workweek has a lot of suggestions on how to put your micro business on autopilot.

If you launched a micro business per week I guarantee you that eventually you'd hit something that pays and a side income stream would take a significant amount of time off your retirement date.

I know that Joe Dominguez and Vicki Robin, the authors of "Your Money or Your Life", fit your criteria. (At least, Joe would if he were still with us.)

For housing, they each rented rooms with friends for parts of their lives. For eats, gardening and swapping food. For travel, cover by honoraria and grants and stipends in support of whatever product or cause merits leaving home.

Source: personal conversations within the "YMoYL" sphere of influence

Oh yes, there is lots you can do to purse FIRE right now.

The first and most important is to learn to enjoy yourself without spending much money. If you can be happy and live the life you want right now at your current income level, it's going to be easy to just keep going at your current spending when you make more.

Next up is education. You should at a minimum read "Your Money or Your Life" and "The Boglehead's Guide to Investing." I suspect that you'd really enjoy the "Early Retirement Extreme" book as well.

After that - experience. I worked as Linux admin for 10 hours a week in college for a couple of years. When it comes down to "years of experience" on a job application, that counts and it can help you get more senior positions or better pay. When you apply to jobs, think about how the job title will look in the future and what skills you can pick up along the way. I'd take Linux Admin for $10/hr any day over Help Desk Technician for $12/hr. This helps you get right past the "entry level" positions and into senior positions straight out of college. My first real IT career job was at a senior level.

As for the car - ouch. What a money pit! It doesn't seem like you can get rid of it due to loans, but driving it less will keep the repair bills down. If paying the loan off early and selling it is in the cards, you might do that before you build up the emergency fund. If you can live without a car for a few months, you can probably buy the next one cash.

12k/year from 150k nest egg is 8%. i don't think annuities go that high.

https://www.schwab.com/annuities

i put in fixed annuity in schwab's online estimator and looks like 4% not adjusted for inflation.

On #2, yes the bum must also pay the SS taxes, so he'd need some money. He'd pay FICA, which includes Medicare tax. When he's eligible for SS he's also eligible for Medicare starting at age 65. The Medicare tax pays for part A of Medicare, which is hospital insurance. The $513/year figure I gave above also pays for Utah state income tax and federal tax.

The answer for #1 is probably yes, in the long run. If it costs < $6k total to generate enough income to qualify for both SS and Medicare, it seems likely a profitable method. Say the average age of death is 85, and he starts SS at age 62. Even if SS paid only $30/month in today's dollars he'd come out ahead. The benefit formula is complex and I'm no expert on this. Here is some data from 2016. It looks like the benefit would be > $210/month after 15 years of contributions, and the benefit of $41/month shown there might require 11 years of contributions.

I don't know whether the roulette method works for generating income for FICA contributions. Also, thinking about this some more, I think taxes would need to be paid quarterly, like self-employed people do, and the taxes would be higher since there's no employer paying half of the Social Security tax. The bum would need to be disciplined to qualify for SS/Medicare this way.

Sure: https://www.fool.com/investing/general/2015/12/13/3-charts-that-show-why-warren-buffet-loves-geico.aspx and https://www.quora.com/How-does-Berkshire-Hathaways-insurance-float-work are some pretty good sources beyond Buffet's shareholder letters.

Geico makes a profit of $1.2B off of $20B in revenue. So that's around a 5% profit margin. They spend another $1B on advertising revenue. So maybe 10-15% gets lost to profits, advertising and overhead?

As for the fire insurance, your house might burn down the day after you sign the agreement, but the actual disbursements to contractors and for materials to rebuild your house takes months or years.

I'm a bot and the movie you linked is called How to Live Forever, here's some Trailers

>the major expense is getting to figure out who is single in the first place

The major expenses I have had are a couple of beers at local brew pub and a Match.com subscription for dating. Tinder is a wasteland right now and even Bumble is getting worse.

​

The more superficial the more superficial the people you will find on there.

What country are you in? From what you describe I think M1 Finance would be perfect for you. I think the App Store describes the features best:

https://play.google.com/store/apps/details?id=com.m1finance.android&hl=en_CA&gl=CA

And the website:

Did you know that when you exercise you’re stimulating/strengthening your central nervous system? If you knew the benefits you’d never stop working out.

Yeah. This was the recent description. I have PTSD and anxiety and some other issues. My troubles at work led me to want to FIRE but you can't run from yourself.

Adult Children Secrets of Dysfunctional Families: The Secrets of Dysfunctional Families

Friel Ph.D., John C.

Which clippers did you buy that allow you to fade your own hair? Do they have the taper lever? I bought this Wahl last year but it doesn't have a taper lever, so I'm not sure I can do a fade with it. Wahl Ultra Close Cut Pro Clipper #79111-1301

Those are nice beginner clippers.

The ones I have cost me around $100 CAD and I got them about 18 months ago. These ones are practically the same ones that I have but are a newer colour/model: https://www.amazon.ca/Wahl-Clipper-Fade-Haircutting-79445/dp/B0798ZGJR5

Good point; I've been using NordVPN the past year or two after switching from somebody else (can't really remember, I think it might have been BTGuard). It's really cheap, I think I paid $60 or something for three years of service. Use it frequently when staying at AirBnBs, Coffee shops, etc.

Oh and I now live outside the US much of the year so it's also super helpful when certain sites want you to access from a US IP address.

They are delicious. You can buy the same ones they have on the planes on Amazon here: https://smile.amazon.com/Daelmans-Stroopwafels-Wafers-Hexa-Ounce/dp/B01ITYGFHA/ref=sr_1_1_a_it?ie=UTF8&qid=1538143139&sr=8-1&keywords=strupwaffel

You didn't list a savings rate so I can't speak to the viability of your plan. I'm guessing your savings rate is decent since your expenses total $32k, but if you aren't making over $60k you should put some effort into the income generation side of that equation.

The first step would be to come up with a budgeting system that works for you and your husband. Your Money or Your Life has a great one, or you can just do all cash spending and take out money each week, or use YNAB or Personal Capital or a Spreadsheet or just a plain old notebook. Whatever it is, it has to make sense to you both.

Next up is the 21 Day Makeover at Early Retirement Extreme. If you are the "rip it off like a bandaid" type person then you can do it in 21 days. Otherwise you could do it a little more slowly.

When we started our journey, I'd pick 2-3 categories each month, determine the absolute minimum spending level for it and then just tried it for a month. Cell phone was a $5/mo dumb phone, haircut was the $16 haircut down the street, cable tv minimum was canceled, you get the picture. I'd just ask What is the absolute least I could spend in this category? Some things that seem essential to your happiness just turn out to be completely optional. You may even find out that spending on it less improves your happiness. From there, we'd adjust the next month and repeat until we felt like the spending was just right.

On a personal level (won't work for everyone) I spent a lot of effort turning my job that I didn't really like into one that I do really like. I got a lot of ideas from So Good They Can't Ignore You and The 4-Hour Workweek and implemented them over a few years until now what I do is impactful, creative and interesting.

To make a long story short, instead of fixing the mess I now build automation to fix the mess. I also stopped going to meetings, moved some responsibilities to other team members and I'm putting more effort into training.

Cal Newport wrote a series of books about career that have a lot of practical advice. So Good They Can't Ignore You is a good one - he advocates becoming skilled at something the world desperately needs and then you can use that to set the conditions of your working life.

The books that stuck with me are below and I have asterisks in the spreadsheet. They are diverse and got me to where I am in a pretty short time.

Frugal gazette is a bit dated, but the author's story and their ideas got me into frugality. Author retired on little with her husband and she was a controversy about "depriving" her kids.

Personal Finance for Dummies: Eric Tyson is great. He really provides the insight into finance. And its fun to read. He's a bit radical for many by saying to save for retirement and not fund kids college (he explains why).

The Millionaire Next Door - people with money often don't change their lives and they don't flash it around. They live simple. My neighbors are like this.

How to Retire Happy, Wild and Free: Fun and really inspired me to look at retirement in the face. Like people talk about retirement, but they don't really discuss it.

The Little Book of Common Sense Investing. Great book. Don't worry about individual funds, choose your risk level and buy index funds. Index funds beat the pros 80% of the time and index funds are cheaper than the pros and boutique funds.

Early Retirement Extreme - pretty extreme, but you see a side to savings and retiring that is an eye-opener.

Your Money or Your Life - I'm reading it for the 3rd time. It's a great way to re-evaluate your relationship with money. It's like deprogramming from consumerism. There's a new edition coming soon and Mr. Money Mustache talks about the original Mr. Mustache, Joe Dominguez.

I'd love to do that. I'm always a little skeptical about how passive those income streams are. Affiliate marketing requires page views which requires good content and good content takes time.

I'd probably do something more along the lines of The $100 Startup where I try to start something that can bring in cash without a ton of upkeep. At some point I want to do a challenge where I launch 12 micro businesses in 12 months to push myself to actually get something out there.

The more likely answer is that I might hunt for contract jobs where I work for 6 months and hold out until I get one that pays a ton. Then I'd do a solo 401k to bank as much as I can of it. I figure a real job might not be so bad if you are only doing it for 6 months. By the time the new job excitement wears off, you are done.

Head down to the library and get two books: Your Money or Your Life and The Boglehead's Guide to Retirement. Those two books cover all of this, especially the tax avoidance, and you can definitely retire at 45. The strategy isn't significantly different for a younger age, there are ways to access your retirement money before you hit retirement age. Since those books were written, a new product has hit the market offered by Bettermint, Schwab and WealthFront that take your goals as input and then automate the Boglehead's plan. You might decide to use one of those providers, but you should first read the Boglehead's book so that you understand what you are buying.

Also keep in mind that being financially independent doesn't mean you have to be retired early. There are a lot of benefits to having your expenses covered by your own investments rather than your employer. It gives you the leverage to take a few months off, the ability to pick a lower paying dream job and the courage to say no when asked to do something that goes against your ethics. If you were really into it, you could probably be financially independent in about 5 years while still living a pretty normal life.

For now, start tracking your expenses today using Personal Capital. Stop gambling with the 3X ETFs, just cash out your Robinhood account and put it in a savings account and make that the beginning of your emergency fund.

You should get serious about it today. I was basically in your shoes, making $100k a year, living in an apartment that cost $800 a month and money management didn't seem important because the bank account filled up faster than I could empty it. Budgeting has a bad connotation - it's really just a plan to spend your money in the way that gives you the most enjoyment.

Never stop learning about saving money, frugality, investing. Stick to your guns, your plans, adjust them as you need to. Set your goals. Don't borrow money (except for house). Read all of the "retired early" books you can for wisdom. Read the early-retirement websites, although some of those people may have had good paying jobs. Max your 401k, and IRA if you can. Get that house and rent out rooms or build accessory dwelling unit.

You can do it. Just keep at it. Read Your Money or Your Life. Once you have your plan, it's easier to set and forget at some point and not dwell on it. The journey is the destination.

Remember to have some fun. We cook at home, eat at home, drive old cars, delay gratification, don't even think about shopping anymore, go to store when we need to. We do travel a couple of times a year. I don't care for stuff, but like to see places, even if that museums at home or abroad. Read, watch movies, take walks, have hobbies...enjoy life.

Read The Bogleheads Guide to Investing. Even if you do choose an advisor, you still need to understand what you are doing. After you read the book you'll probably realize that the advisor just isn't worth the fee.

If you do seek advice, follow the Bogleheads advice to seek out a fee only advisor with a fiduciary duty towards you. If they don't have a fiduciary duty, they are just salesmen for financial products and are likely to direct you towards high fee products that line their own pockets.

I like the way Your Money or Your Life develops a strategy for this: write down how much you spent in each category and decide if you spent more or less than you wanted to. I'm working on that right now; I've really pulled back my expenses to the detriment of my social life. To attempt to solve this, I'm probably going to take classes to meet people and develop skills.

Maybe read So Good They Can't Ignore You by Cal Newport. I think it gives pretty good career advice, some of which is echoed by people in this thread.

That's one of the best books written about personal finance in my opinion. Too many books try to treat personal finance as some sort of add-on to your actual life rather than an integrated part of it. This one captures the reality that your use of time and money are fundamently connected and should be treated that way.

The investment advice is poor and lacks detail, especially if you are reading the older edition published in the 70's when US bonds were paying massive amounts of interest due to inflation. It's a book about saving, not investing - stick to a Boglehead's book for that.

A Random Walk Down Wall Street is a great book too, but it's not going to give you any clues on how to make your life more meaningful. It's just about turning money into more money.

I never realized that you could retire early. I never really cared for the big house or fancy car or spending money, but it didn't click that I could be done working far before traditional retirement age.

I got a career job, I bought a small house, I got married and paid for a wedding and all of the sudden money was just a lot tighter before. Before it used to just kinda pile up in the checking account faster than I really spent it, but now I needed to be on top of it. I read /r/personalfinance (back in the day when it was fiercely anti-debt), found a reading list and went through it.

Boglehead's Guide to Investing made me realize that I could turn money into more money, Your Money or Your Life made me realize that I could retire a lot earlier than 55. Looking at the example of Jacob from ERE helped me understand that even 5 years was possible if you changed your mindset.

I guess Jacob would be my role model. My wife has nicknamed him the "cheap bastard" but not in a bad way. Personally, I'd dive headfirst into an Jacobesk existence, but my wife prefers a more traditional existence.

> Next up is education. You should at a minimum read "Your Money or Your Life" and "The Boglehead's Guide to Investing." I suspect that you'd really enjoy the "Early Retirement Extreme" book as well.

Sorry, could you tell me if these are worth a look into for an European as well, or do these books pertain mostly to Americans?

50? I don't mean to age discriminate but I've never been at a social event with someone older than in their 40s, except for family events. Like it would be a completely different vibe being at say a halloween party, kegs, red cups everywhere and people almost of AARP age. Maybe a professional event, but that's different. I mean I very rarely see older people at the bars and clubs I go to, from my understanding there are bars with older crowds.

I seriously have never heard of that. The oldest person in my pretty large social group (30+ people) is 38 I believe...then goes as young as 25.

IDK might be the social circle though. Like if its a hiking group for meetup.com, yeah there will be more age variation.

Where do you find these clubs? I'm not retired but I would really like to get involved with something like that. I've tried Meetup.com but every group seems to fizzle out after a few months due to lack of interest/attendance except for the ones focused on going out to bars.

Maybe tell them you're not buying anything for them for a while and they have to earn the money. You can pay them to do jobs around the house, or help them figure out something to do outside the house.

Is that considered child abuse now? Kids (at least on Reddit) seem to live rather cushy lives. At 14 I got special papers to work 'under-age' because I wanted/needed cash. My father was a tyrant with the purse, and a bit of a dick; but I don't see a good way to inspire without actual need.

'Hustle' culture doesn't seem to be as trendy these days. Now they're all 'lying flat'. Which I have to say, I find less annoying. We have a rich history of loafing, and I see it coming back in fashion. Here's an enjoyable book on the subject.

ive got a bidet that is like a kitchen sink sprayer that attached to the water intake for the existing toilet, it was like $30.

like this: https://www.amazon.com/Handheld-Toilet-Adjustable-Pressure-Feminine-Stainless/dp/B086W1YZSH

Read The Simple Path to Wealth by JL Collins to learn how to invest and manage your finances. How to Achieve Financial Independence and Retire Early is a useful listen too.

TD;LR - Invest (ideally) 50% of your income into VTSAX (US total market index fund) whilst working at a well-paying career for 10 years, then you'll have enough money to retire (with a stash equalling 25 times your annual income from which you withdraw around 4% every year).

Honestly, this book changed my life:

The Millionaire Next Door: The Surprising Secrets of America's Wealthy

I found it in the public library. Cheaper used copies are likely available on eBay.

The easiest way to convert between British and American:

| American | British | |

|---|---|---|

| Traditional 401(k) | SIPP / Workplace pension | Contributions are made before income tax, tax on withdrawals |

| Roth 401(k) | ISA | Contributions are made after income tax, withdrawals are untaxed |

However you have to be aged 59½, and have held the account for five years, to withdraw from a Roth 401(k), which is not the case with an ISA.

https://www.schwab.com/resource-center/insights/content/roth-vs-traditional-401-k-which-is-better

https://www.schwab.com/ira/inherited-ira/withdrawal-rules

I'd probably use the Life expectancy method if that's still an option for you.

Generally if you are using the 10 year method, you'd withdraw roughly an equal amount each year. You'd probably start with more than 10% (like 15%) of the balance because it will likely grow over the 10 years. That will keep your tax bracket relatively stable.

As for personal finance, the source of the money doesn't matter when it comes to spending it. If you are required to take a distribution it doesn't matter if you use it to pay your electric bill or put it in a brokerage account, all the matters is your overall savings. You would do the same thing with it that you'd do with a bigger paycheck - contribute to a Traditional IRA or HSA if you can, otherwise deposit it into a brokerage account and buy index funds.

If you go this route, I highly highly recommend these noise canceling headphones. Very cheap, work great, I've given them away as gifts. I actually have a pair I bought during black Friday for $32, but now with the coupon they're giving they're $30.

Only thing is one person had a ear cuff/pad come out. They superglued it back in place.

My wife bought me a coffee mug warmer that eliminated my dependence on microwaves AND ensured my cup in the morning is always hot! AMAZING life-changing purchase under $30.

Haha that’s funny, you telling me to research. Have you ever taken out Roth contributions before? I have. No penalty when filing taxes next year.

Here’s a source for you: https://www.schwab.com/ira/roth-ira/withdrawal-rules

What you’re thinking of is the 5 year minimum time in order to withdraw earnings tax free for an eligible expenses (like buying a home)

https://www.schwab.com/ira/roth-ira/withdrawal-rules

You can withdraw contributions to a Roth IRA anytime tax and penalty free. There are a number of exemptions where you can withdraw the earnings tax and penalty free if you've had it longer than 5 years (see website above). The 5 year clock starts when you open the account, not from when you put money in.

So opening the account and funding it with some trivial amount (to keep it open, some places will close accounts with a 0 balance) starts the clock.

Best part is opening the account now, going to college for 4 years to get a degree, and then getting a job to start putting money away is going to take you ~5 years and thus you'll never have to care about not having a Roth IRA less than 5 years.

Schwab is showing no minimums. Shouldn't really have issues IMO.

https://www.schwab.com/public/eac/account_features/brokerage_account

Fees and commissions

Open an account with a $0 minimum deposit plus get $0 online equity trade commissions, regardless of your account balance or how often you trade.

I'm a tall guy that is kind of built like a gorilla, so I consume a lot of calories. Close to 3000 a day to maintain my weight. I track my nutrition with https://cronometer.com/ ...if you are not familiar with that site you should take a look. It is really great and the free version is really all you need. You can set your macros to where you want, but it makes sure you are getting everything you need. If you need more of a food diary breakdown I'll see if I can put something like a monthly shopping list together for you.

Do a SSO / OAuth sign-in instead if you need sign-in / accounts. Super easy to implement now days.

I had my devs look at Firebase Authentication a while back, and he got it running and working in about an hour. We were all blown away. It's free for unlimited web login IIRC. Works with Google, iOS, Facebook, Twitter, etc... https://firebase.google.com/docs/auth/web/google-signin

>Try it while only making $54,000.

Wish I had that problem. Try it while only make $31,000.

>I refuse to have a car. It is something that I am adamant about building my life around and others say that I am crazy or that eventually I will have to get a car

Hey if that works for you rock on, but not everyone lives in San Freattle York City where such a thing is possible. Grocery is more than a mile from my house, work is 5ish miles and this weekend it was in the 90's with 80-90% humidity. Friends and family start at 5 miles and branch out to 25 miles away. So when you say things like:

>because of the way middle class americans judge those without cars and are shocked if you don't have one. And all the other consumer crap and mind numbing entertainment they push on us.

Is pretty narrow-minded. I assume you live in a city where you can get by without a car, it's just not going to happen here in most of Indy and many many many other places around the country (and world).

>Personally I feel that this has a small return relative to what a business owner could make.

About half of all new establishments survive five years or more and about one-third survive 10 years or more. those aren't great success rates and that doesn't even touch how much are actually making wortwhile profits considering time invested. That also seems to only look at small businesses that have employees, I imagine 1-man operations fail far more often because most of the time it's nothing more than someone forming an LLC and hanging their shingle out with no real government agency getting info about success/failure rate except the IRS seeing a possible change in one's taxes.

u/Appropriate_Snow_742

They make better quality ones, but these are cheap and are very popular. I have one, and it doesn't use much power or fuel: Diesel Heater

There's gasoline ones too, which can be plumed right into your gas tank. But you could buy a few cheap ones for the cost of one quality heater.

Before making a Roth IRA withdrawal, keep in mind the following guidelines, to avoid a potential 10% early withdrawal penalty:

Withdrawals must be taken after age 59½.

Withdrawals must be taken after a five-year holding period.

There are exceptions to the early withdrawal penalty, such as a first-home purchase or college expenses.

From the Schwab website

https://www.amazon.com/Book-Strategies-Savvy-Estate-Investor-ebook/dp/B01BWDHLTQ/

You need a CPA who specializes in real estate. This book is available on Scribd via a free one month trial.

Millionaire Expat: How To Build Wealth Living Overseas https://www.amazon.co.uk/dp/B078TR1FLP/ref=cm_sw_r_apan_glt_9F7JWXPP8M5FRXJ5T6W4?_encoding=UTF8&psc=1

Here are some good points on how to invest from different regions of the world.

We're neighbors BTW (Moldova)

Anyone thinking about Robinhood should do more research on its SPIC coverage first (think FDIC for stock brokerage). I duckduckgo "robinhood spic" and the first link is a Bloomberg article questioning this dated December of 2018, relatively recent.

Robinhood itself says its SPIC insured here though. And even if they have insurance, recent news suggest they are definitely a bit more on the likely side of something going wrong and bankruptcy. And just because there is insurance it can still be quite a pain if you end up having to deal with it.

I think most people going for RE have several buckets to withdraw from, and will set aside the retirement accounts until they hit that age. However, with a ROTH IRA you are able to withdraw your contributions at anytime without penalty, and only your earnings would be subjected to taxes and penalties. For example, if you put $1,000 into a roth, and it grows to $1,500, you can take out your original $1,000 without penalty.

​

Here's a good explanation: https://www.schwab.com/public/schwab/investing/retirement_and_planning/understanding_iras/roth_ira/withdrawal_rules

I've been using Wallet by BudgetBakers for some time now. I track everything manually using the free version. It has the option to categorise expenses/income and set budgets. I also use the tags to specifically mark out where I've been spending money.

It also has an online webapp which is nice to have which also lets you upload .csv bank statements to populate your records.

The free version is good enough for my purposes right now, but if you do buy the premium version, you get unlimited accounts (I think free is limited to 3) and you can sync data with your bank.

Hey! I'm in Europe and I've been living in a van for the past two years.

Parking is no problem here, it's easy to find places where you're accepted, and authorities are mostly nice.

This is an awesome life with more freedom I could ever imagine. And as your main goal suggest, it's so cheap!

I shared some of my experience here: https://www.indiehackers.com/post/one-year-as-a-nomad-entrepreneur-d989e51bd2

You can generally set up most things through the website. Once you have an account, they have secure messaging that they use.

Can you use some sort of VoIP product to make phone calls? Something like Google Duo?

Well, the good thing is that you recognise you're doing this.

> I haven't figured out what I want to do with my life

This is what you have to figure out.

I'm a string believer that you have to pick the one thing that's important to you - doesn't matter what it is - and make it your priority. I used to fly paragliders pretty seriously (and every day) and now I sail - for you it could be something completely different.

You might find the book Your Money or Your Life helpful.

There's a wiki page of book recommendations too - I'd recommend it to OP.

People on here can probably summarise the passive investing methodology in a few sentences, but in my opinion reading a book gives a fuller and deeper understanding - Tim Hale's <em>Smarter Investing</em>, which is aimed at a UK audience) was what made it all "click" for me. There's quite a lot to understand if you want to be confident and feel comfortable sitting through a market crash.

You can also get this book for $3 or so (i.e. the price of shipping credits). It's an excellent primer into those countries: